Table of Contents

Most people save too little, and unknowingly spend too much. The 50/30/20 Rule of Budgeting & saving 2025 for budgeting is a way to become more aware of your financial habits and limit overspending and under-saving (by spending less on the things that don’t matter to you, you can save more for the things that do).

Because this is just a rule of thumb for planning your budget you’ll also need to supplement it with a system to monitor spending.

What is the The 50/30/20 Rule of Budgeting & saving 2025?

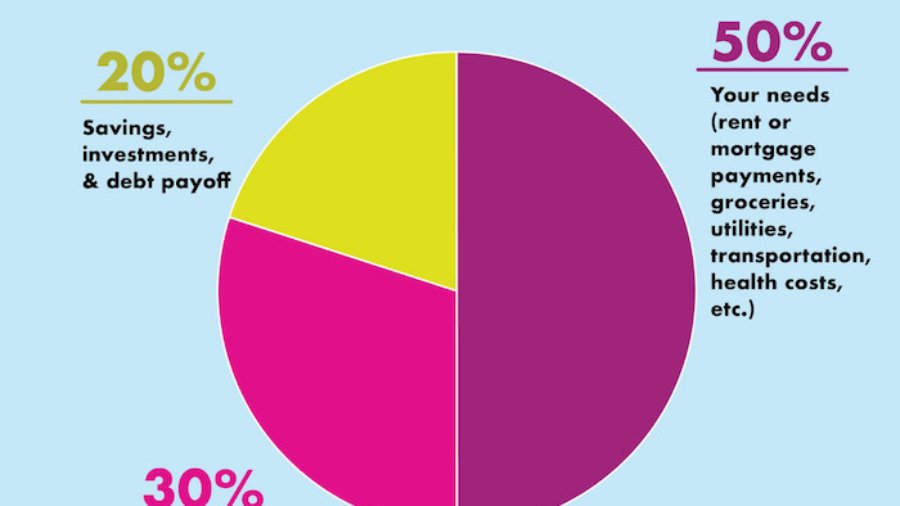

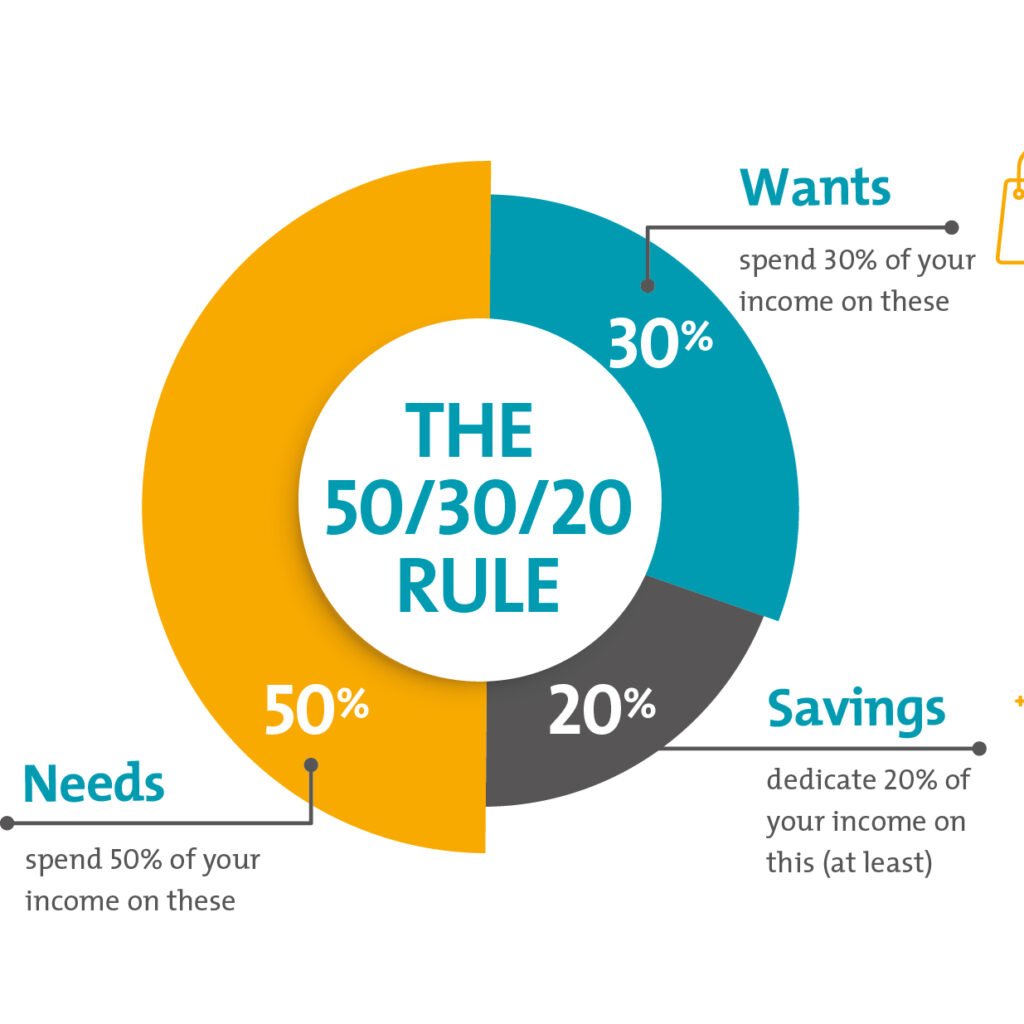

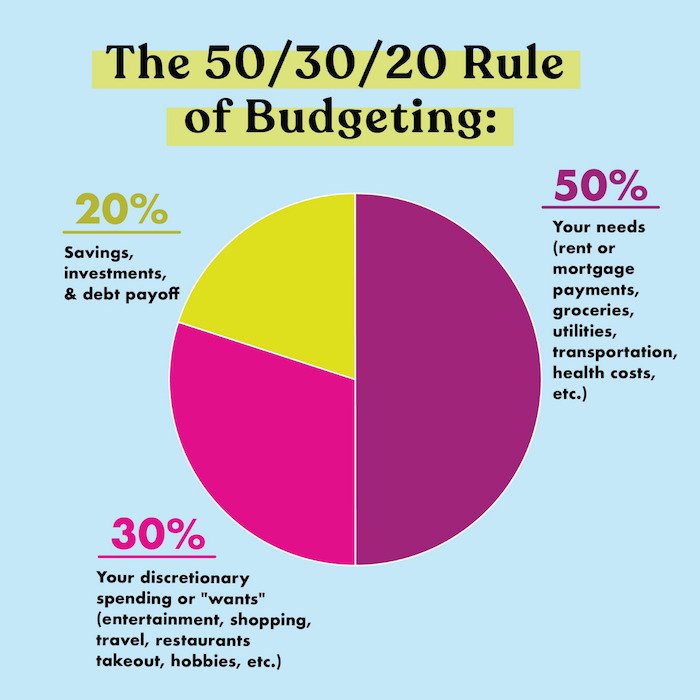

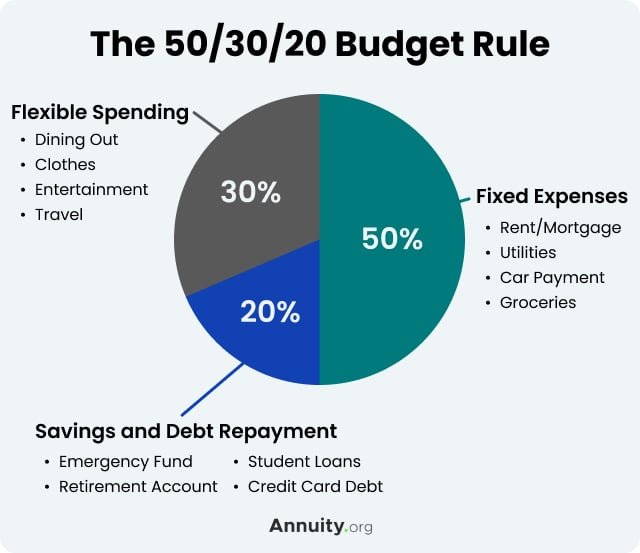

The 50/30/20 Rule of Budgeting & saving 2025 is a guideline for allocating your budget to three categories, ‘needs’, ‘wants’ and financial goals as follows:

50% to Needs

Needs are what you can’t live without, or at least very easily. They include things like:

- Rent/Mortgage payments

- Groceries

- Utilities, such as electricity and water

30% to Wants

Wants are things that you desire but don’t actually need to survive. They might include:

- Hobbies

- Holidays

- Dining out

- Digital and streaming services like Netflix and Amazon.

20% to Financial Goals

This category includes savings and money set aside for debt payments.

How to use The 50/30/20 Rule of Budgeting & saving 2025

- Calculate your monthly income. Add up how much guaranteed income you receive in your bank account each month.

- Calculate a spending threshold for each category: Multiply your take-home pay by 0.50 (for needs), 0.30 (for wants), and 0.20 (for financial goals) to see how much you should ideally spend in each category.

- Plan your budget around these numbers: Think of these three categories as “buckets” that you can fill with monthly expenses. List and tally your monthly expenses under the category each falls into and see if you’re spending less than the monthly targets you established in the prior step.

- Follow your budget: Track your expenses each month, and make changes where needed, in order to stick to your spending thresholds going forward

The 50/30/20 Rule of Budgeting & saving 2025 vs. Other Budgeting Methods

The 50/30/20 Rule of Budgeting & saving 2025 of thumb isn’t the only game in town. Here are a few other budgeting techniques to consider:

80/20 Rule: With this method, you immediately set aside 20% of your income into savings. The other 80% is yours to spend on whatever you want, no tracking involved.

Advantages of The 50/30/20 Rule of Budgeting & saving 2025

Simplicity: Its greatest strength is its simplicity. It’s easy to understand and implement, making it perfect for budgeting beginners who are intimidated by more granular methods.

Flexibility: The rule uses broad categories, which gives you flexibility in your spending. You don’t have to track every single penny in dozens of subcategories. As long as you stay within your three main buckets, you’re on track.

Promotes Balanced Financial Health: It forces you to prioritize savings and debt repayment by dedicating a significant 20% of your income to these goals. At the same time, it builds in a 30% allowance for “wants,” preventing the burnout that can come from overly restrictive budgets.

Disadvantages of The 50/30/20 Rule of Budgeting & saving 2025

Challenging in High Cost of Living (HCOL) Areas: In expensive cities, housing and other “needs” can easily consume more than 50% of income, making the rule difficult to follow without significant sacrifices.

Not Ideal for Irregular Income: For freelancers or those with variable paychecks, basing the percentages on a fluctuating income can be challenging.

May Not Be Aggressive Enough for High Debt: If you have substantial high-interest debt, the 20% allocation might not be aggressive enough. In this case, a more debt-focused approach may be necessary.

Compared to a method like zero-based budgeting, where every single dollar is assigned a “job,” the 50/30/20 rule is less rigid. Zero-based budgeting offers more control and precision but requires significantly more time and effort to maintain. For many, the 50/30/20 rule provides a “good enough” structure that is easier to stick with long-term.

How to Apply The 50/30/20 Rule of Budgeting & saving 2025 With Low Income

A common criticism of this rule is that it doesn’t work for everyone, especially those with lower incomes. Learning how to apply 50/30/20 with low income requires creativity and flexibility, but it can still be a valuable guideline.

The key is to treat the percentages as a goal, not a strict law.

Adjust the Percentages: If your needs exceed 50%, don’t give up. You might need to adjust to a 60/20/20 or even a 70/15/15 split temporarily. The priority is to cover your needs first, then ensure you are still saving something—even a small amount—before allocating to wants.

Focus on Cutting “Wants” First: When money is tight, the “wants” category is the first place to look for cuts. This could mean canceling subscriptions, cooking at home more often, or finding free entertainment options.

Protect Your Savings Goal: Even if you can only save 5% or 10% of your income, make it a priority. Paying yourself first, no matter how small the amount, builds a crucial financial habit. Automate this transfer on payday so you aren’t tempted to spend it.

Case Study Example:

Maria earns $2,200 per month after taxes. A strict 50/30/20 split would be $1,100 (Needs), $660 (Wants), and $440 (Savings). However, her rent and utilities alone cost $1,200.

Instead of abandoning budgeting, she adjusts. Her “Needs” are closer to 60% ($1,320). She decides to keep her savings goal at 20% ($440) as she wants to build an emergency fund. This leaves her with 20% ($440) for “Wants” and all other variable expenses for the month. It’s tight, but by focusing on free social activities and cooking at home, she makes it work.

Alternatives to the 50/30/20 Rule

If the 50/30/20 framework doesn’t feel right for you, don’t worry. There are many other effective budgeting methods. The best one is always the one you can stick with consistently. Here are a few popular alternatives to the 50/30/20 rule:

Zero-Based Budgeting: As mentioned, this method involves assigning a purpose to every single dollar you earn. Your income minus your expenses should equal zero at the end of the month. It’s perfect for meticulous planners who want maximum control over their money.

The Envelope Method: A classic cash-based system. You withdraw cash for your variable spending categories (like groceries, gas, entertainment) and put it into labeled envelopes. When the envelope is empty, you’re done spending in that category for the month. It’s highly effective for curbing overspending.

The 70/20/10 Rule: This is a variation often recommended for those who want to prioritize saving and investing more aggressively. It allocates 70% to spending (both needs and wants combined), 20% to savings, and 10% to debt repayment or investing.

You might choose an alternative if you have a very specific goal, such as rapid debt elimination, or if you find the broad categories of the 50/30/20 rule too vague.

Practical Tips to Stick With the Rule

Creating a budget is one thing; sticking to it is another. Here are some tips to help you stay on track.

Automate Your Savings: This is the most powerful trick in the book. Set up an automatic transfer from your checking account to your savings or investment account every payday. This “pays yourself first” and ensures your 20% goal is met without relying on willpower.

Use Apps to Track Your Expenses: Use a budgeting app (like Mint, YNAB, or your bank’s built-in tools) to automatically categorize your spending. This makes it easy to see where your money is going and whether you’re staying within your 50/30/20 targets.

Review and Adjust Monthly: Your budget isn’t set in stone. Life happens. A car repair or an unexpected bill can throw things off. Review your spending at the end of each month. See what worked and what didn’t, and adjust your plan for the next month accordingly.

FAQs Of The 50/30/20 Rule of Budgeting & saving 2025

What is the 50/30/20 budget rule in simple terms?

In simple terms, it’s a rule of thumb for managing your money. You divide your after-tax income into three parts: 50% for essential needs (like rent and groceries), 30% for non-essential wants (like hobbies and dining out), and 20% for savings and paying off debt.

Is the 50/30/20 budget realistic?

For many people, yes, it is very realistic because of its simplicity and flexibility. However, it can be unrealistic for those in very high cost-of-living areas or for individuals with very low incomes or extremely high debt, as their “needs” may take up a much larger portion of their income.

Can I use the 50/30/20 rule with debt?

Absolutely. The “20%” category is explicitly for Savings and Debt Repayment. If you have high-interest debt, like from credit cards, you should prioritize paying it down within this 20% category. Once your high-interest debt is gone, that entire 20% can be shifted toward savings and investing.

What is better than the 50/30/20 rule?

There is no single “better” budget; the best budget is personal. A zero-based budget might be better for someone who needs strict control over every dollar. The envelope system might be better for someone who struggles with overspending on debit or credit cards. The 50/30/20 rule is often best for beginners who need a simple, balanced starting point.

Conclusion

Mastering your money doesn’t have to be complicated. The 50/30/20 budget rule offers a powerful, accessible, and balanced approach to financial management. By dividing your income into Needs, Wants, and Savings, you create a clear roadmap for your spending that aligns with your financial goals. It provides structure without being overly restrictive, empowering you to cover your bills, enjoy your life, and still build a strong financial foundation for the future.

While it may not be the perfect fit for every single person, it serves as an excellent starting point. Give it a try for a month or two. Track your spending, see how it aligns with the 50/30/20 ratios, and make adjustments as needed. You might find that it’s the simple framework you’ve been looking for to finally achieve financial peace of mind.

{kind=link}