Business directories are online platforms that compile and organize information about various businesses. They typically include details like the business name, address, phone number, website, and other essential data.

They serve as digital repositories where consumers can search for specific products, services, or businesses within a particular geographic area or niche.

For several reasons, getting your business listed in such an online directory is crucial.

This article delves into the Top 5 B2B Directory Platforms In Europe In 2025, highlighting their unique features, services, and contributions to the business ecosystem.

Choosing the right business directory can make or break your European market expansion. With over 500 million potential customers across 27 EU member states, you’d think finding quality directories would be straightforward. It’s not. The European business directory ecosystem is fragmented, multilingual, and surprisingly complex.

In 2025, Business-to-Business (B2B) platforms have become indispensable for companies aiming to expand their reach, streamline operations, and foster global partnerships.

Europe, with its diverse market and robust technological infrastructure, hosts several leading B2B platforms that cater to various industries.

Top 5 B2B Directory Platforms In Europe In 2025

After extensive testing across 15 European markets, these Top 5 B2B Directory Platforms consistently deliver results for international businesses. Each platform offers unique advantages depending on your target market and business model.

1. Wer liefert was(wlw.de) (Germany)

The undisputed champion of European B2B directories. With 3 million company profiles across 45 countries, it is a well-established B2B directory in Europe. It facilitates interactions between businesses and potential partners, suppliers, and clients.

wlw.de Europe’s leading B2B marketplace, wlw connects businesses with over 3 million verified suppliers, across 45 countries, offering tools like multilingual search, and RFQ (Request for Quote). Get QUOTE for your business

It has gained prominence among buyers, brands, manufacturers, suppliers and enterprises looking to broaden their networks and form meaningful business relationships.

Wer liefert was(wlw.de)facilitates over €1 billion in annual trade connections, Their advanced search algorithms and verified supplier network make them needed for manufacturing and wholesale businesses.

wlw.de (Wer liefert was)

wlw.de is a leading European B2B marketplace connecting buyers with verified suppliers across industrial, manufacturing, and technical sectors.

Key Features

- Detailed supplier profiles with products and certifications

- Product- and industry-specific B2B search

- RFQ tools for direct buyer–supplier communication

- SEO-optimized listings for higher visibility

- Performance analytics and lead insights

Pros

- Trusted brand among European procurement professionals

- High-intent B2B audience

- Strong fit for industrial and technical suppliers

- Effective lead generation channel

Cons

- Premium visibility requires paid plans

- Competitive categories may reduce exposure

Extra Information

Best suited for manufacturers, wholesalers, and service providers targeting professional buyers in Germany and Europe.

What advantages does wer liefert was (wlw) offer suppliers?

wer liefert was (wlw) is the leading B2B marketplace in Europe offering suppliers, manufacturers, distributors, and service providers unique opportunities to enhance both visibility and business growth.

Building trust through a strong network

As part of an established marketplace, you are recognized as a credible provider. Buyers know that wlw represents quality and reliability.

Increased visibility with potential customers

Each month, wlw connects you with 400,000 buyers from industry, commerce, and the service sector. An optimized company profile that effectively showcases your products and services increases your exposure to key decision-makers.

Enhanced online presence

Leverage the reach of wlw to boost your visibility in search engines like Google. Our platform provides additional exposure through SEO-optimized content and targeted advertising.

Targeted lead generation

With user-friendly search functions and precise categorization, buyers can easily find your offerings—helping you win qualified inquiries.

2. Kompass

Originally French, now covering 70+ countries with particularly strong European presence. Kompass excels at detailed company information including financial data, key executives, and trade references. Premium features include tender notifications and market intelligence reports.

Kompass is a global B2B information provider with a strong presence in Europe. It offers a comprehensive database of companies, enabling businesses to find and connect with potential partners, clients, and suppliers.

Kompass

Kompass is a global B2B database providing structured company data, supplier insights, and decision-maker information.

Key Features

- Detailed company and industry classification

- Global B2B supplier database

- Advanced search and filtering tools

- Decision-maker and firmographic data

- CRM and sales intelligence support

Pros

- Highly structured and reliable data

- Strong for B2B sales and prospecting

- Global company coverage

- Useful for market research

Cons

- Premium access required for full data

- Less focused on inbound lead generation

Extra Information

Kompass is ideal for sales teams, analysts, and enterprises focused on data-driven B2B prospecting.

Key Features:

Verified Business Listings: The platform ensures credibility by verifying company information before listing them in its directory.

Global Business Directory: Kompass provides detailed company profiles, including financial information, business activities, and contact details.

Targeted Marketing Solutions: Businesses can use Kompass for lead generation, email marketing, and digital advertising to reach their target audience.

Sector-Specific Search: The platform categorizes businesses based on industry, making it easier for users to find relevant suppliers and partners.

Data-Driven Insights: Kompass offers analytics and reporting tools that help businesses make informed decisions.

3. Europages

Europages is a leading European B2B directory that connects businesses across various sectors. With a multilingual platform, Europages facilitates international trade by providing detailed company profiles and product information.

Europages

Europages is a pan-European B2B directory connecting buyers with manufacturers, exporters, and service providers across international markets.

Key Features

- Multilingual supplier profiles

- International product and company search

- SEO-friendly business listings

- Export-focused visibility across Europe

- Category-based supplier discovery

Pros

- Strong international reach

- Supports cross-border B2B trade

- Recognized European business directory

- Useful for exporters and manufacturers

Cons

- Lead quality varies by industry

- Premium plans needed for higher exposure

Extra Information

Europages works best for companies targeting multiple European markets and international buyers.

Key Features:

Verified Reviews: Users can access and provide reviews, fostering a transparent and trustworthy business environment.

Multilingual Support: Europages supports multiple languages, breaking down communication barriers and enabling businesses to connect across different regions.

Detailed Company Profiles: Businesses can create comprehensive profiles, including product catalogs, certifications, and contact information, enhancing visibility.

SEO Optimization: The platform optimizes profiles for search engines, increasing the likelihood of discovery by potential partners.

Trade Opportunities: Europages regularly updates trade opportunities and tenders, providing businesses with avenues for growth and collaboration.

4. Yellow Pages Europe

Yellow Pages Europe is a long-established business directory network that helps companies across European markets increase visibility and connect with potential B2B and B2C customers. Originating from traditional printed directories, it has evolved into a digital-first platform offering online business listings, local search visibility, and advertising solutions. For B2B companies, it serves as a discovery channel where buyers can find suppliers, service providers, and partners by industry and location.

Key Features

Yellow Pages Europe typically offers searchable online business listings, company profiles with contact details, categories by industry, and location-based search. Many versions also support enhanced listings, allowing businesses to add descriptions, logos, photos, operating hours, and website links. Additional features may include local SEO support, paid advertising placements, analytics on listing performance, and integration with maps or mobile apps to improve reach among local and regional audiences.

Pros & Cons

The main advantages of Yellow Pages Europe include strong brand recognition, credibility, and usefulness for local and regional B2B discovery, especially for small and medium-sized enterprises. It can improve online visibility and generate inbound leads without heavy technical setup. However, limitations include varying traffic quality depending on country, competition within popular categories, and reduced impact compared to modern B2B marketplaces or intent-driven platforms. Paid listings can also become costly, and results may be less measurable than advanced digital marketing channels.

5. eWorldTrade

eWorldTrade has emerged as a pivotal player in the European B2B marketplace, connecting millions of buyers and suppliers across the continent. Established with the vision of simplifying international trade, eWorldTrade offers a comprehensive digital platform that facilitates seamless transactions, communication, and collaboration between businesses.

Key Features:

- Extensive Product Directory: eWorldTrade boasts a vast catalog encompassing a wide range of products and services, enabling businesses to find suitable partners effortlessly.

- Verified Suppliers: The platform ensures credibility by featuring verified manufacturers and suppliers, thereby fostering trust and reliability in business dealings.

- Advanced Search Filters: Users can leverage sophisticated search filters to pinpoint specific products or services, enhancing the efficiency of the procurement process.

- Secure Payment Options: eWorldTrade integrates secure payment gateways, ensuring safe and transparent financial transactions.

- Trade Shows and Events: The platform regularly organizes virtual trade shows and events, providing businesses with opportunities to showcase their offerings and network with potential partners.

Conclusion

In conclusion, the Top 5 B2B directory platforms in Europe in 2025 demonstrate how digital marketplaces have evolved into essential tools for sustainable business development and cross-border trade. These platforms play a decisive role in helping companies increase visibility, generate qualified leads, and connect efficiently with professional buyers. Choosing the right directory is no longer just about presence, but about partnering with a platform that delivers trust, relevance, and measurable commercial impact.

Within this competitive landscape, wlw.de (Wer liefert was) clearly emerges as the most compelling B2B directory and business marketplace for industrial and technical sectors. Its strong reputation, verified supplier ecosystem, and consistently high buyer intent position it as a preferred platform for serious B2B growth. For companies targeting the European market—particularly Germany—wlw.de offers a powerful combination of credibility, reach, and lead quality, making it a standout choice and a strategic investment for businesses aiming to strengthen their market position in 2025 and beyond.

Boost Credit Score: 10 Best Proven Ways to Boost Your Credit Score Fast in 30 Days

Introduction: Ready to Boost Your Credit Score Fast?

Have you ever checked your credit score and felt that sinking feeling—it’s lower than you thought? You’re not alone. Whether you’re planning to buy a home, get a car loan, or simply qualify for better credit card rates, improving your credit score can make all the difference.

The good outcomes is You can raise your credit score fast—sometimes even Boost your credit score in 30 days—by following the right strategies. In this post, we’ll uncover 10 proven ways to give your score a serious boost and get you closer to financial freedom.

check your credit status/Report with FREE legit tools verified by international credit Bureaus:

1. GROWCredit.com Free credit analyser

2. creditkarma.com get unlimited credit checking&reporting

Overview: Key Credit Score Boosting Features

| Feature | Action | Timeframe |

|---|---|---|

| Credit Utilization | Reduce below 30% | Within 30 Days |

| Payment History | Pay bills on time | Immediate Impact |

| Disputes | Fix errors on credit report | 2–4 Weeks |

1: 3 Immediate Actions to Boost Your Credit Score Fast

If you need to increase your credit score in 30 days, start with these quick wins:

Three way to Raise your credit score fast within 30 days

- Pay down credit card balances – Reducing your credit utilization ratio below 30% can cause a rapid score jump.

- Ask for a credit limit increase – A higher credit limit with the same balance lowers your utilization instantly.

- Become an authorized user – Ask a family member with great credit to add you to their card.

These actions can help Boost your credit score fast, often within weeks.

2: How to Understand Your Credit Report (Step-by-Step)

To increase your credit score, you must first know what’s hurting it.

Follow these steps to get your free credit report:

- Visit AnnualCreditReport.com — the only official free source.

- Request your report from Equifax, Experian, and TransUnion.

- Review all accounts for errors, late payments, or unknown inquiries.

By understanding your report, you can take targeted steps to raise your credit score fast and fix mistakes that may drag it down.

3: Dispute Errors: Step-by-Step Process + Free Template

Errors happen more often than you think.

A single mistake could lower your score by 50+ points! if the following steps didnt solve your issue contact us here with Free help.

Here’s how to fix it:

Step-by-Step to Dispute Errors

- Identify the incorrect entry on your credit report.

- Gather proof (bank statements, receipts, etc.).

- Submit a dispute directly with the credit bureau online.

Free Email Template:

Subject: Request to Remove Incorrect Entry from My Credit Report

Dear [Credit Bureau],

I recently reviewed my credit report and found an inaccurate item: [describe issue].

Please investigate and remove this error. Attached are supporting documents.Thank you,

[Your Full Name]

[Your Address]

[Last Four Digits of your SSN]

Disputing incorrect items can significantly increase your credit score in 30 days once corrected.

4. Strategic Credit Utilization Moves

Credit utilization accounts for 30% of your FICO score. To raise your credit score fast, aim to keep utilization low.

- Pay off high balances before the statement date.

- Spread balances across multiple cards.

- Use balance alerts to track usage.

Credit Utilization Tips Table

| Tip | Effect on Score | Result Time |

|---|---|---|

| Pay down 50% of balances | +20 to +50 points | 1 Month |

| Request higher limits | +10 to +30 points | 2 Weeks |

| Set up auto-pay | Prevents dips | Ongoing |

5. Use Credit Builder Tools & Products Wisely

Tools like credit-builder loans or secured cards can help raise your credit score fast, especially if you’re rebuilding.

Pros & Cons Table

| Tool | Pros | Cons |

|---|---|---|

| Credit Builder Loan | Reports payments monthly; builds history | Small upfront deposit required |

| Secured Credit Card | Easy approval; reports to bureaus | Requires security deposit |

| Rent Reporting Service | Adds positive data fast | Usually a monthly fee |

6. Set Realistic Timeline Expectations

While you can raise your credit score fast, the exact improvement depends on your credit profile.

- Minor fixes (like utilization) can improve your score in 2–4 weeks.

- Major issues (like late payments) may take 3–6 months to recover.

For example, Sarah raised her credit score 80 points in 30 days simply by paying down credit cards and disputing one error.

7. Monitor Progress & Stay Consistent

Use a credit monitoring tool (like Experian, Credit Karma, or SmartCredit) to track your score weekly. Monitoring helps you spot issues early and celebrate your progress.

Ready to track your credit growth? Try this credit monitoring tool →

Conclusion: Your 30-Day Path to a Better Credit Score

Raising your credit score doesn’t have to take years. By applying these 10 proven methods, you can increase your credit score in 30 days—or even sooner.

Remember, the key to success is consistency and awareness. Check your report, manage utilization, and use credit wisely. You’ll be surprised how fast results show up.

Start today and see how quickly you can raise your credit score fast toward your financial goals!

FAQs: Raise Credit Score Fast – Common Questions Answered

1. Can I really increase my credit score in 30 days?

Yes! Paying down balances, correcting report errors, and lowering utilization can show results within a single billing cycle.

2. What’s the fastest way to raise my credit score 100 points?

Combine multiple tactics: pay down debt, remove errors, and use credit-builder tools.

3. Does checking my credit score lower it?

No. Checking your own credit is a soft inquiry and doesn’t affect your score.

4. How often should I check my credit report?

Review it every month, especially if you’re trying to raise your credit score fast.

5. Are credit repair companies worth it?

They can help, but you can often do the same steps yourself for free using the methods above.

How to Start Investing in Europe 2025: Expert-Driven Guide to Building Wealth Over Time

Introduction

Ever wondered why some people seem to grow their wealth effortlessly while others struggle to save? The truth is, the difference often lies in how they invest.

As Europe’s financial markets evolve rapidly, knowing How to start investing in Europe 2025 has become one of the smartest moves for anyone looking to secure their financial future.

Whether you’re in Amsterdam, Berlin, Madrid, or any corner of the European Union, this comprehensive guide will walk you through everything you need to know to begin investing with confidence.

The European investment landscape offers unique opportunities and challenges, from navigating different tax systems across EU member states to understanding the regulatory framework that protects investors

In this guide, we’ll break down exactly where and how to invest — from stocks and ETFs to real estate and digital assets — so you can start building long-term wealth confidently, even if you’re a complete beginner.

Why Investing in Europe in 2025 Matters More Than Ever ?

Financial literacy is one of the most important subjects and one that can have the greatest impact on your life. Unfortunately, it is something rarely taught in schools.

The European market is entering a powerful new phase. With inflation cooling, interest rates stabilizing, and digital finance platforms expanding, over the past decade Europe’s economic landscape has evolved significantly thus making investing not just beneficial, but essential for long-term financial health, indeed investing in Europe in 2025(How to start investing in Europe 2025) offers diverse opportunities across industries and countries.

Why 2025 Is the Year to Invest in Europe(top 5 reasons pointing How to start investing in Europe 2025)

- Stronger regulations ensure more transparent markets.

- Sustainable investing (ESG) is booming with tax incentives.

- Low entry barriers through online brokers and mobile investing apps.

- Increasing returns in green energy, AI, and fintech sectors.

- Moreover, European investors now enjoy more access to global ETFs, fractional shares, and crypto assets — tools that were once reserved for professionals.

Where & How to start investing in Europe 2025

Before you invest a single euro, define why you’re investing; Is it for retirement, passive income, or financial independence?

Step-by-step approach:

- Define your goal. Example: €100,000 net worth in 10 years.

- Decide your risk tolerance. Conservative, balanced, or aggressive.

- Pick your investment horizon. Short-term (1–3 years) or long-term (10+ years).

- Create an emergency fund. At least 3–6 months of expenses before investing.

This roadmap helps align your investments with your life priorities — and keeps you disciplined when markets fluctuate.

Best Investment opportunities in Europe 2025

Let’s look at the most promising and accessible options for European investors this year.

Quick Overview Table

| Investment Type | Features | Pros | Cons | Expert Tips |

|---|---|---|---|---|

| ETFs | Diversified, low-cost index funds | Low fees, easy access | Market risk | Start with MSCI World ETF for global exposure |

| Stocks | Direct ownership in companies | High potential returns | Requires research | Focus on blue-chip dividend stocks |

| Real Estate/REITs | Property-based income | Inflation hedge | Illiquidity risk | Try REIT ETFs for diversification |

| Green Investments | Eco-friendly and ESG-focused | Long-term stability | Lower short-term gains | Check EU Green Deal projects |

| Crypto | Blockchain-based assets | High upside | Volatility | Invest less than 10% of your portfolio |

1. Exchange-Traded Funds (ETFs)

ETFs remain the go-to choice for beginners due to low fees and diversification. You can invest in European indices like the Euro Stoxx 50 or global funds like MSCI World.

Pros:

- Diversified exposure

One ETF can give investors exposure to many stocks from a particular industry, investment category, country, or a broad market index. ETFs can also provide exposure to asset classes other than equities, including bonds, currencies, and commodities.

- Low costs

ETFs, which are passively managed, tend to have significantly lower expense ratios than actively managed mutual funds. What drives up a mutual fund’s expense ratio? Costs such as a management fee, fund accounting and trading expenses, and load fees related to their sale and distribution

- Trades Like a Stock

An investor requesting a mutual fund redemption during the trading day can’t really be sure of the redemption price. That will depend on where the fund’s net asset value lands when it’s calculated at the end of the day. In contrast with mutual funds, ETFs:

- May serve as underlying securities for option contracts

- Trade at a market-based price updated throughout the trading day

- Can be purchased on margin and sold short

The most popular ETFs trade with more liquidity than most stocks. This means that there are always plenty of buyers and sellers and narrow bid-ask spreads.

- Immediately Reinvested Dividends

The dividends of the companies in an open-ended ETF are reinvested immediately, whereas the exact timing for reinvestment can vary for index mutual funds. (One exception: Dividends in unit investment trust ETFs are not automatically reinvested, thus creating a dividend drag.)3

- Limited Capital Gains Tax

ETFs can be more tax-efficient than mutual funds. As passively managed portfolios, ETFs (and index mutual funds) tend to realize fewer capital gains than actively managed mutual funds.

Mutual funds, on the other hand, are required to distribute capital gains to shareholders if the manager sells securities for a profit. This distribution amount is made according to the proportion of the holders’ investment and is taxable.

If other mutual fund holders sell before the date of record, the remaining holders divide up the capital gain and thus pay taxes even if the fund overall went down in value.4

- Lower Discount or Premium in Price

There is a lesser chance of ETF share prices being higher or lower than those of underlying shares. ETFs trade throughout the day at a price close to the price of the underlying securities, so if the price is significantly higher or lower than the net asset value, arbitrage will bring the price back in line.

Unlike closed-end index funds, ETFs trade based on supply and demand, and market makers will capture price discrepancy profits.5

U.S. Securities and Exchanges Commission. “Mutual Funds and ETFs.”

- Fast Fact

One minor risk of ETFs (though not unique to them) is shutdown risk, or the risk that an ETF will close. While shareholders would get their money back, there can be annoyances other than having to reinvest your money.

These can include capital gains taxes that investors are unprepared for and potentially unexpected fees.

Cons:

Market volatility

In the dynamic world of investing, market volatility serves as both a signal and a stress test. It reflects the degree of variation in asset prices over time and captures the emotional pulse of investors navigating uncertainty. Periods of heightened volatility often emerge from shifts in macroeconomic indicators, geopolitical tensions, or sudden market shocks. While such fluctuations can unsettle even experienced investors, they are also the crucible where new opportunities are forged. Understanding volatility is not just about weathering turbulence—it’s about interpreting the rhythm of market behavior and aligning strategies with changing tides.

Returns depend on global trends

The interconnectedness of global markets means that returns increasingly depend on international trends. A slowdown in China’s manufacturing sector, a change in U.S. interest rates, or a breakthrough in renewable energy technologies can send ripples across equity and bond markets worldwide. Investors no longer operate in isolated economies; they navigate a global ecosystem where currency movements, trade policies, and emerging market growth collectively influence performance. Recognizing these macro patterns allows investors to anticipate shifts rather than merely react to them, positioning portfolios to benefit from structural global transformations.

Strategic Adaptation in an Uncertain World

Professional investors understand that volatility and global trends are not adversaries but essential elements of modern finance. The key lies in strategic adaptation—diversifying across regions and sectors, using hedging instruments, and staying informed through continuous macroeconomic analysis. By balancing short-term defensive moves with long-term conviction, investors can transform volatility from a source of anxiety into a source of alpha. Ultimately, navigating global trends is less about predicting every move and more about building resilient strategies that thrive amid constant change.

2. Stocks and Dividends

European stock markets (Germany’s DAX, France’s CAC 40, or London’s FTSE 100) offer solid dividend-paying companies.

To start:

Open an account with a regulated broker (like., DEGIRO, Trade Republic, or Interactive Brokers).

Research companies with strong fundamentals and dividend history.

Reinvest dividends for compounding growth.

3. Real Estate & REITs

You don’t need to buy property physically. In 2025, Real Estate Investment Trusts (REITs) allow investors to access property income with minimal effort.

Why it’s great opportunity

- Strong rental demand in cities like Lisbon, Berlin, and Warsaw.

- Inflation hedge and stable cash flow.

4. Sustainable & Green Investments

Green bonds, solar funds, and eco-ETFs are rising fast. The EU Green Deal supports eco-projects, making sustainable investing in Europe 2025 both ethical and profitable.

5. Crypto & Digital Assets

For those seeking higher risk and innovation, regulated exchanges like Bitpanda or eToro Europe offer access to crypto assets. Always diversify and never invest what you can’t afford to lose.

| Investment Type | Features | Pros | Cons | Expert Tips |

|---|---|---|---|---|

| ETFs | Diversified, low-cost index funds | Low fees, easy access | Market risk | Start with MSCI World ETF for global exposure |

| Stocks | Direct ownership in companies | High potential returns | Requires research | Focus on blue-chip dividend stocks |

| Real Estate/REITs | Property-based income | Inflation hedge | Illiquidity risk | Try REIT ETFs for diversification |

| Green Investments | Eco-friendly and ESG-focused | Long-term stability | Lower short-term gains | Check EU Green Deal projects |

| Crypto | Blockchain-based assets | High upside | Volatility | Invest less than 10% of your portfolio |

How to Build Your First Portfolio

Now that you understand the options, let’s create a beginner-friendly portfolio for 2025.

- Start small — even €50/month works.

- Diversify — combine ETFs, stocks, and one alternative (REIT or crypto).

- Automate — set up recurring monthly investments.

- Rebalance — review your portfolio every 6–12 months.

- Stay consistent — long-term investing beats market timing.

Top Tricks to Succeed in European Investing & Exploring How to start investing in Europe 2025

- Use Euro-based brokers to avoid currency conversion fees.

- Track your progress using portfolio apps like JustETF or Portfolio Performance.

- Educate yourself through EU financial literacy portals or YouTube finance experts.

- Join local investor communities for tips and insights.

- Stay updated with economic trends and ECB policy changes.

Common Mistakes to Avoid

- Investing without an emergency fund.

- Panic selling during market dips.

- Ignoring diversification.

- Overexposure to crypto or risky assets.

- Following “get rich quick” advice.

Conclusion

Starting your investing journey in Europe in 2025 doesn’t require a finance degree — just the right mindset and consistent habits. Begin small, stay disciplined, and focus on long-term growth over short-term excitement.

By following the expert-driven strategies above, you can confidently navigate the European market and build a portfolio that grows your wealth steadily over time.

Ready to take the next step?

Read our guide on Best European ETFs for Beginners in 2025 or explore Top Robo-Advisors for Passive Investing.

Experian review 2025 (Best Guide of CreditWorks & IdentityWorks You Should Read: )

Experian review 2025| What is Experian what does Experian do?

our Guide today(Experian review 2025) focus one of the leading in credit business and activities,Experian is one of the three major credit bureaus in the US, alongside TransUnion and Equifax, It offers credit monitoring, score tracking, and identity protection services with different levels of coverage we will explain bit by bit our trending topic Experian review 2025.

Experian is a global data and technology company, powering opportunities for people and businesses around the world, by helping to redefine lending practices, uncover and prevent fraud, simplify healthcare, deliver digital marketing solutions, and gain deeper insights into the automotive market, all using unique combination of data, analytics and software.

They also assist millions of people to realize their financial goals and help them to save time and money.

We operate across a range of markets, from financial services to healthcare, automotive, agrifinance, insurance, and many more industry segments.

I’ve thoroughly examined Experian’s identity protection products with our research team, Apart from being one of the three primary credit bureaus, Experian has become a significant player in the identity protection industry with its IdentityWorks platform.

In this review(Experian review 2025), I will examine Experian’s credit monitoring services, security protocols, and security features. In order to assist you in determining whether its services are cost-effective and whether recent security incidents should sway your decision, I will carry out extensive testing and analysis.

🌟 Experian Overview

- ⭐ Rating: 4.5 / 5

- 💰 Price: $24.99/ month

- ✅ Free Version: Yes with no limits

- 📱 Platforms: Web, iOS, Android

- 🔔 Credit Monitoring: Included

- 🛡️ Insurance: 1$ million +Identity theft insurance

- ✨ Additional Features: Credit score simulation, alerts, and reporting tools,social security number monitoring

IdentityWorks is now a closed service that can only be accessed with a complementary code. Meanwhile, the IdentityWorks technology appears to have been migrated into the CreditWorks dashboard. So, the normal CreditWorks subscription now includes the full IdentityWorks identity protection technology. For accessibility, I will refer to IdentityWorks and CreditWorks interchangeably throughout this review.

Experian IdentityWorks features

During my testing, IdentityWorks and CreditWorks offered a rich set of features but a few notable limitations. Here’s a closer look at what the service provides:

| Feature | Basic Plan | Premium Plan | Family Plan |

|---|---|---|---|

| Dark Web Monitoring | ✔️ | ✔️ | ✔️ |

| Real-Time Fraud Alerts | ✔️ | ✔️ | ✔️ |

| Credit Monitoring (1 Bureau) | ✔️ | ✔️ | ✔️ |

| Credit Monitoring (3 Bureaus) | ❌ | ✔️ | ✔️ |

| Identity Theft Insurance ($1M) | ✔️ | ✔️ | ✔️ |

| Social Security Number Monitoring | ❌ | ✔️ | ✔️ |

| Bank Account & Credit Card Monitoring | ❌ | ✔️ | ✔️ |

| Lost Wallet Assistance | ❌ | ✔️ | ✔️ |

| Child Identity Monitoring | ❌ | ❌ | ✔️ |

| Daily Credit Score Tracking | ❌ | ✔️ | ✔️ |

| Customer Support (24/7) | ✔️ | ✔️ | ✔️ |

The old pricing model for IdentityWorks was simple: a free plan for basic Experian credit monitoring, a $24.99/month Premium plan for in-depth individual protection, and a $34.99/month Family plan, enough for two adults plus ten children. Each tier adds to features and levels of protection progressively, with paid plans providing critical services like three-bureau monitoring and identity theft insurance. Under the new, combined model, the Family subscription tier has disappeared, and there is only a CreditWorks Basic (free) and CreditWorks Premium option at $24.99/month.

- Free credit reports and scores available

- Trusted by millions worldwide

- Real-time credit alerts and monitoring

- Identity theft protection options

- User-friendly website and mobile app

- Some premium features require a subscription

- Reports may contain outdated information

- Customer service can be hard to reach

- Data breaches have occurred in the past

- Complex cancellation process for subscriptions

According to my testing, Experian’s biggest pros are its extensive monitoring and credit reporting. With a wide range of identity protection features – especially in paid plans – you can find coverage that suits your needs, including some features like court record monitoring and social network spying.

That said, users should be mindful of the operational challenges, including the complex interface and known customer service challenges. Although the recent platform improvements are promising, the expected premium charges have already raised questions regarding the system’s reliability and whether it might affect the overall user experience. It all boils down to whether you care more about complete monitoring than the interface is simple to use and customer support is a prompt response away.

Our methodology

A thorough review takes more than reading promotional materials or skimming other articles. Our specialists have developed and refined specific testing criteria to examine how Experian IdentityWorks performs in real-world conditions. We focus on five key components of identity theft protection, each weighted according to its importance in keeping you safe.

- Protection features (30%). We rigorously test core monitoring capabilities, including three-bureau credit tracking, dark web surveillance, Social Security number monitoring, and financial account protection.

- Monitoring and alerts (25%). Our team evaluates alert speed, accuracy, and customization options by tracking how quickly and reliably the service responds to potential threats.

- Recovery services (20%). We assess the effectiveness of recovery specialists, examine insurance coverage details, and verify the quality of support for credit freezes and fraud resolution.

- User experience (15%). We evaluate platform usability, mobile app functionality, and the accessibility of educational resources through hands-on testing.

- Value for money (10%). We analyze pricing structures against feature sets and compare family plan options with competitor offerings to determine true market value.

How much does Experian cost?

| Feature | Basic Plan | Premium Plan | Family Plan |

|---|---|---|---|

| Free Trial | Free forever (limited features) | 7-day free trial for 1 user | 7-day trial with child ID monitoring (up to 10 kids) |

| Monthly Subscription | Free | $24.99/month | $34.99/month |

| Annual Plan Option | ❌ | ✅ | ✅ |

| Cancel Anytime | ✅ | ✅ | ✅ |

| Family Coverage | ❌ | ❌ | ✅ (up to 10 children) |

| Daily Credit Reports | ❌ | ❌ | ✅ |

| Daily FICO Score Updates | ❌ | ✅ | ✅ |

| Access to Tri-Bureau Credit Data | ❌ | ✅ | ✅ |

| Premium Support Access | ❌ | ✅ | ✅ |

| Lost Wallet Assistance | ❌ | ✅ | ✅ |

These plans offer strong protection, but it’s important to add that competitors like Aura protect five adults and unlimited children for $30/month. For users prioritizing direct bureau integration and robust monitoring capabilities, Experian is worth the price.

key features of Experian review 2025:

- Credit score monitoring: One of the things I liked most about Experian is the chance to get a free credit report. You can check it along with your FICO score without sharing your credit card details.

- Credit reports: Experian also helps you keep track of your credit reports. You can opt for a free credit monitoring service, which gives you daily updates of any credit changes or score drops.

- Dark web surveillance: Experian also comes with a great range of cybersecurity tools, including Dark Web monitoring, which actively looks for your personal information appearing on the Dark Web and sends real-time alerts. While comprehensive cybersecurity tools are available in paid plans, you can also do a quick Dark Web scan for free.

- Credit locking and fraud resolution assistance: Unlike other bureaus, which only offer credit freezing (and it usually takes days to freeze/unfreeze), Experian came up with a neat CreditLock feature. It allows you to prevent unauthorized credit pulls and related activity. Furthermore, you can also set up fraud alerts and receive real-time notifications from a designated fraud resolution agent for further instructions. In worst-case scenarios, Experian keeps you covered with up to $1 million in identity theft insurance.

- FICO score simulator: Instead of just checking your credit score, Experian also helps you run simulations to see how you might improve it. I especially liked playing with all the different options and checking how they would reflect on my credit score, and I find this feature to be useful for most consumers.

Experian review 2025- Experian IdentityWorks-Boost

Experian IdentityWorks features

During my testing, IdentityWorks and CreditWorks offered a rich set of features but a few notable limitations. Here’s a closer look at what the service provides:

| Feature | Basic Plan | Premium Plan | Family Plan |

|---|---|---|---|

| Dark Web Monitoring | ✔️ | ✔️ | ✔️ |

| Real-Time Fraud Alerts | ✔️ | ✔️ | ✔️ |

| Credit Monitoring (1 Bureau) | ✔️ | ✔️ | ✔️ |

| Credit Monitoring (3 Bureaus) | ❌ | ✔️ | ✔️ |

| Identity Theft Insurance ($1M) | ✔️ | ✔️ | ✔️ |

| Social Security Number Monitoring | ❌ | ✔️ | ✔️ |

| Bank Account & Credit Card Monitoring | ❌ | ✔️ | ✔️ |

| Lost Wallet Assistance | ❌ | ✔️ | ✔️ |

| Child Identity Monitoring | ❌ | ❌ | ✔️ |

| Daily Credit Score Tracking | ❌ | ✔️ | ✔️ |

| Customer Support (24/7) | ✔️ | ✔️ | ✔️ |

Experian’s credit monitoring operates through daily scans rather than instant updates, checking for changes across credit files. Premium and Family plan members receive monitoring capabilities that cover all three credit bureaus, while the Basic plan monitors only Experian data. Daily credit reports and FICO scores – on paid plans only – help you track your credit health over time.

Premium plans give you access to reports from TransUnion.

And Equifax as well:

The identity protection suite includes dark web surveillance across 600,000 web pages, though users need to specify which information to monitor.

Experian IdentityWorks Identity Theft Protection Plans and Pricing for 2025

| Feature | Basic Plan | Premium Plan | Family Plan |

|---|---|---|---|

| Free Trial | Free forever (limited features) | 7-day free trial for 1 user | 7-day trial with child ID monitoring (up to 10 kids) |

| Monthly Subscription | Free | $24.99/month | $34.99/month |

| Annual Plan Option | ❌ | ✅ | ✅ |

| Cancel Anytime | ✅ | ✅ | ✅ |

| Family Coverage | ❌ | ❌ | ✅ (up to 10 children) |

| Daily Credit Reports | ❌ | ❌ | ✅ |

| Daily FICO Score Updates | ❌ | ✅ | ✅ |

| Access to Tri-Bureau Credit Data | ❌ | ✅ | ✅ |

| Premium Support Access | ❌ | ✅ | ✅ |

| Lost Wallet Assistance | ❌ | ✅ | ✅ |

These plans offer strong protection, but it’s important to add that competitors like Aura protect five adults and unlimited children for $30/month. For users prioritizing direct bureau integration and robust monitoring capabilities, Experian is worth the price.

How does Experian work?

Experian collates information from a number of different sources, including:

Personal information, such as your date of birth, address and whether you are on the electoral roll.

Existing credit agreements, including how much of your credit limit you are using (known as “credit utilisation”), your track record of making payments on time and any late or missed payments.

Examples of problems with debt include defaults, CCJs, IVAs and bankruptcy. These only appear on your credit report for 6 years before being removed.

Experian doesn’t include information about your employment, salary or income, or health expenses. It does, however, look at how often you apply for credit and whether you have been turned down for credit in the past.

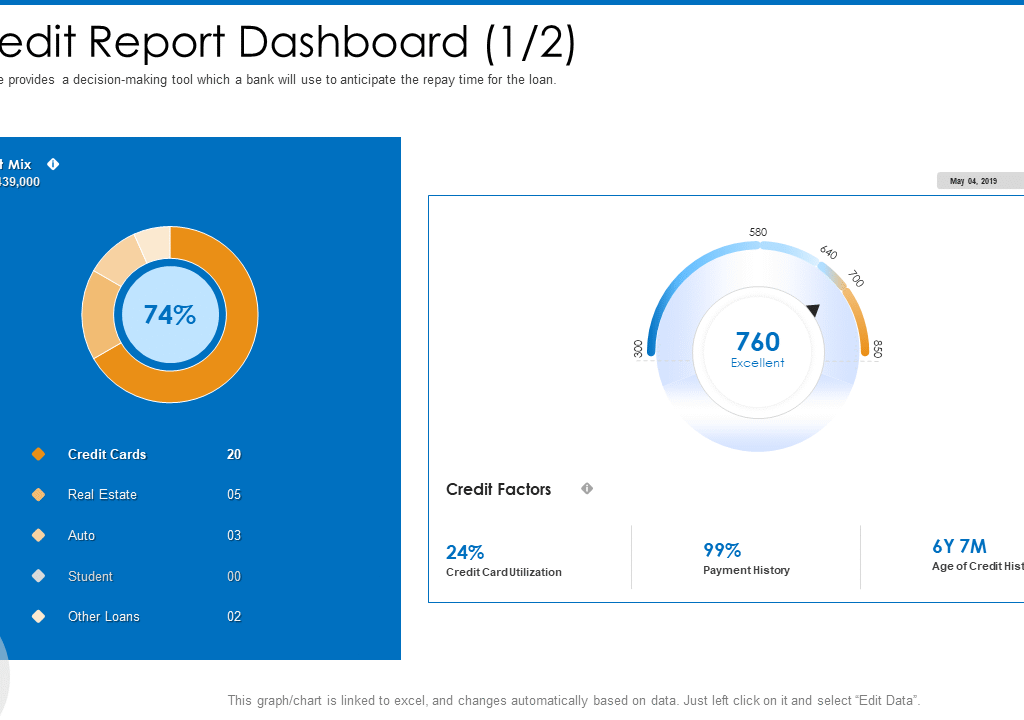

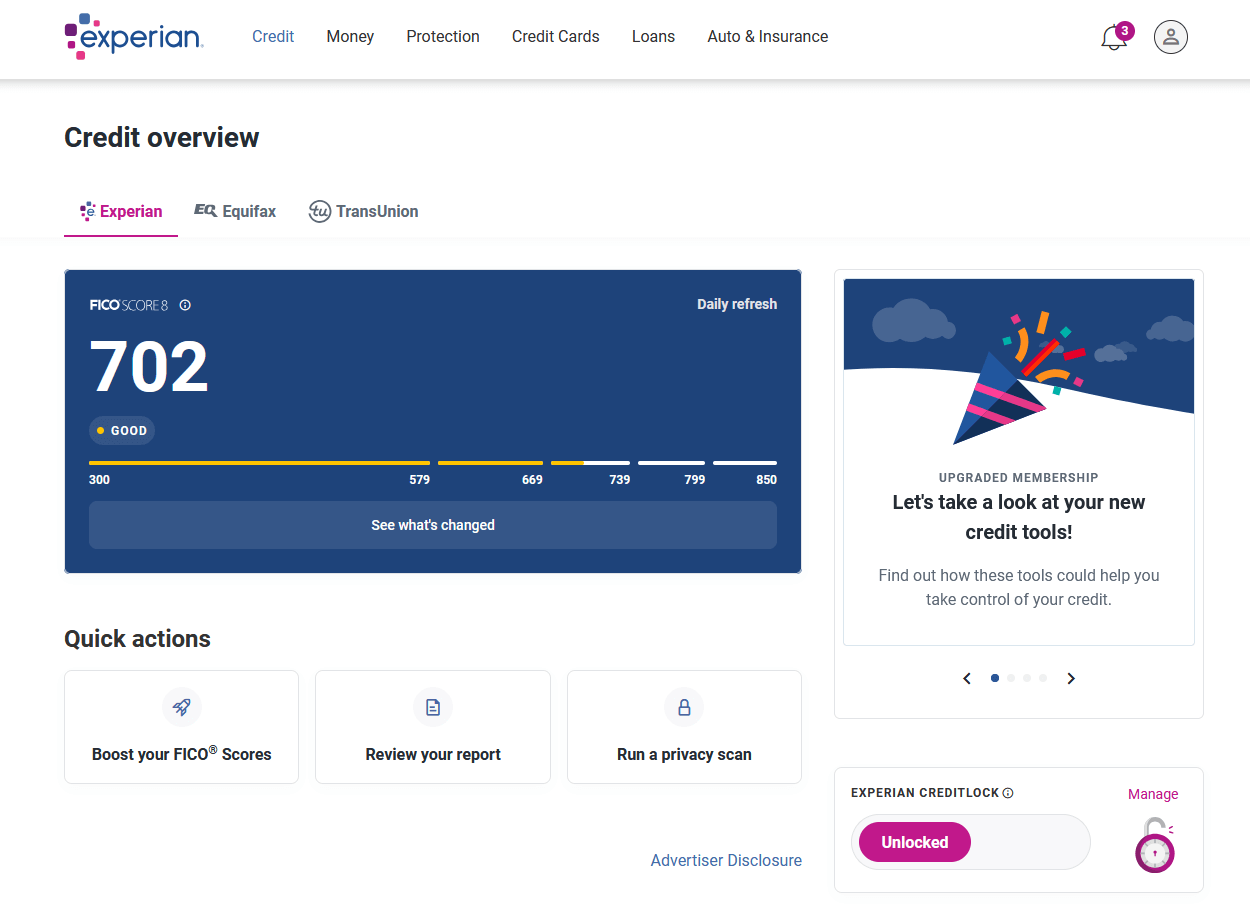

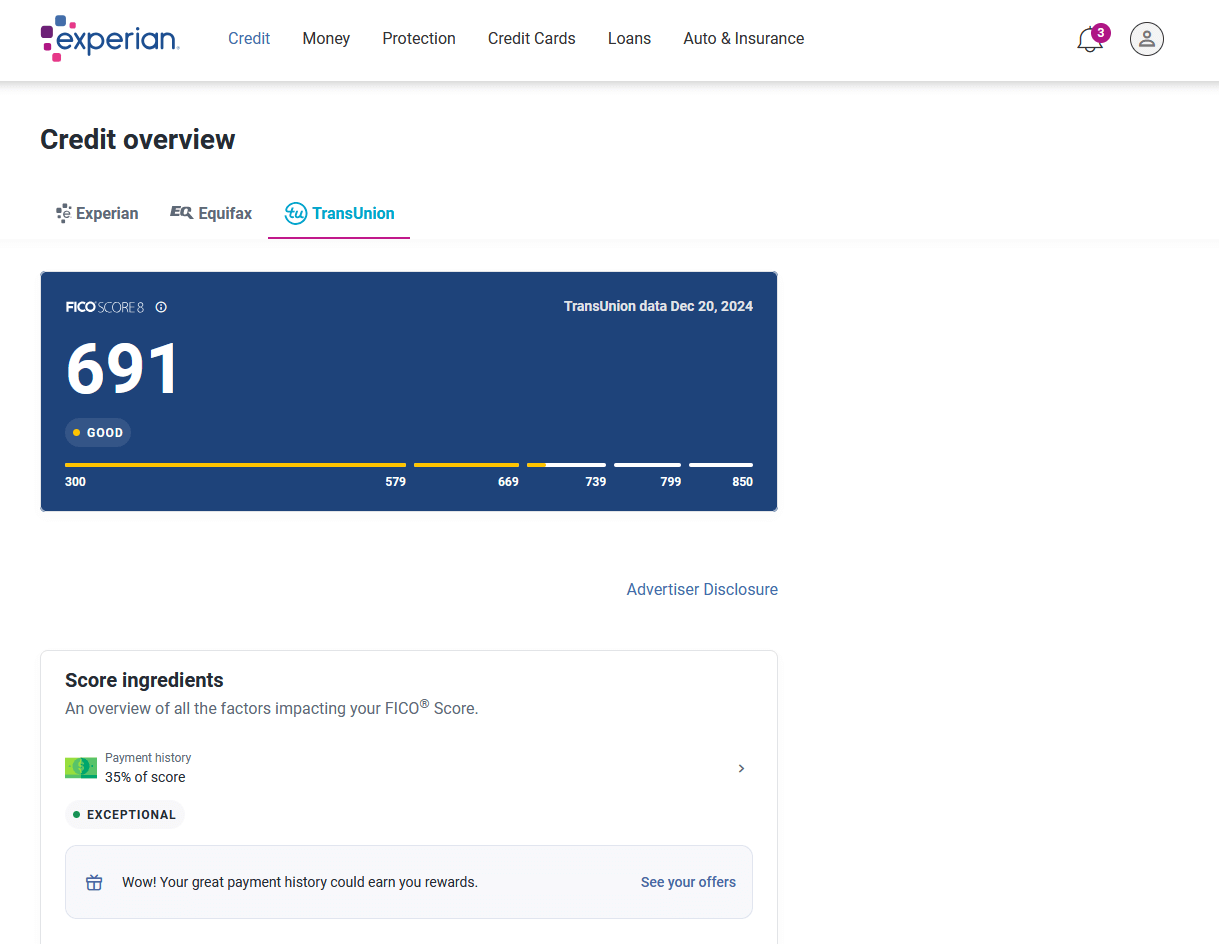

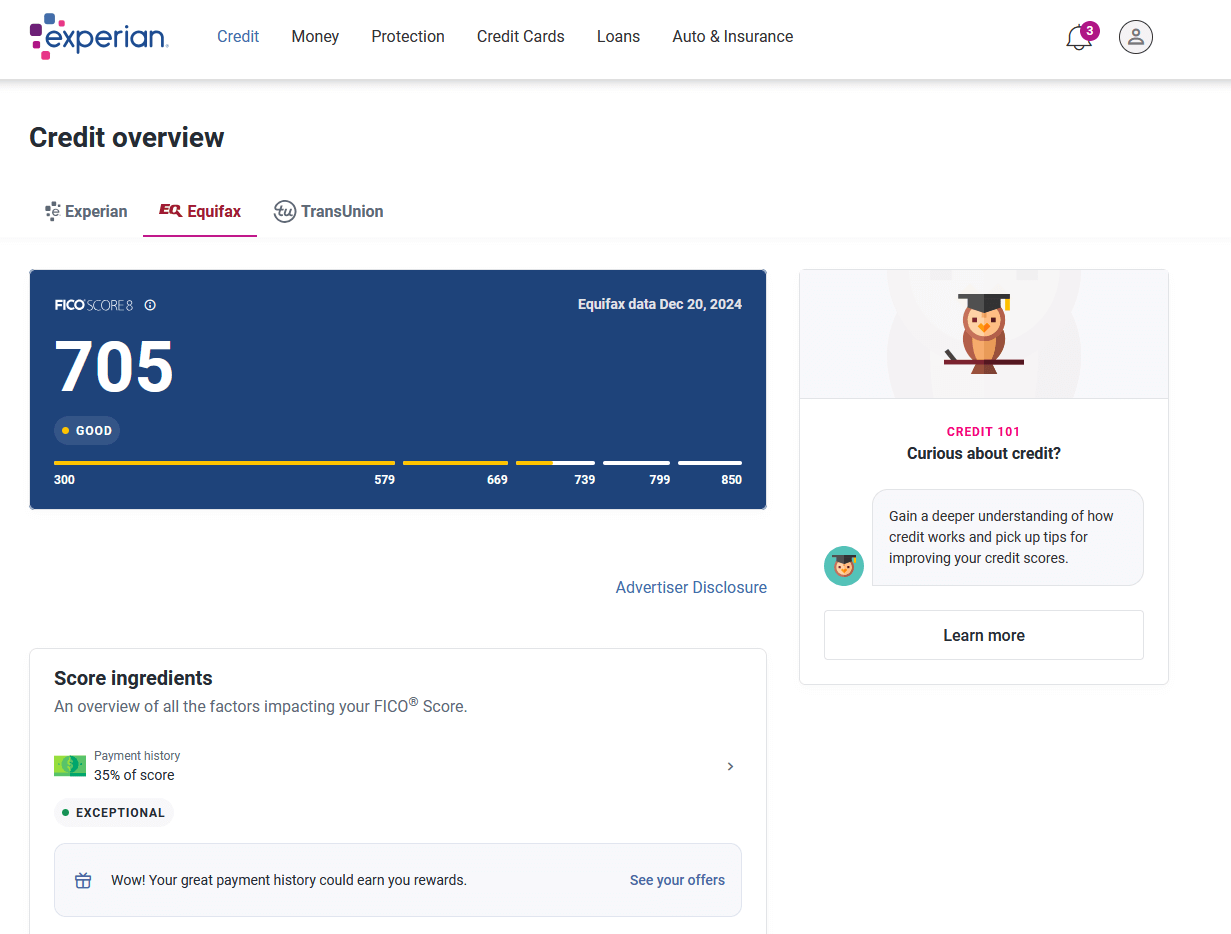

It uses all of this information to come up with a score between 0-999, with 999 being the perfect score. This number gives lenders a guide to your potential creditworthiness, although different lenders will view your score differently rather than there being a one-size-fits-all approach. In short, viewing your Experian credit score, alongside your score with other credit reference agencies, will give you an indication of whether you are likely to be approved for credit, but it doesn’t act as a guarantee.

Experian review ? Free Credit Score Rating

What is the most accurate credit score?

As with other credit reference agencies, Experian uses information collected from official sources and lenders. There is the potential for errors to occur or for out-of-date entries to drag your score down. Experian, Equifax and TransUnion also collect data from different sources, so your report will often vary significantly across all three, including the overall credit score you are given. It is, therefore, worth checking your report with all three providers, correcting any errors and making a note of the overall credit score for each. This is all the more important as you can’t be sure which of the providers’ reports lenders will use when you apply for products in the future. You could, for example, have checked your Experian score, but the lender refers to the Equifax report, which could have a different overall credit rating that makes you less likely to be accepted.

How to ensure accuracy

Dispute errors: If you find errors, file a dispute with the credit bureau to have the information corrected.

Check all three reports: You are entitled to a free credit report from each bureau (Experian, Equifax, and TransUnion) every 12 months at AnnualCreditReport.com.

Review for errors: As you check your reports, look for any inaccuracies, such as incorrect personal information, accounts that don’t belong to you, or wrong payment statuses.

Why Experian may differ from other Credit Agencies(Services)

- Reporting schedules: Lenders do not report to all three bureaus at the exact same time, so credit reports can have different information at any given moment.

- Data sources: Each bureau may receive information from a different set of creditors, leading to variations in the accounts listed on each report.

- Scoring models: While Experian uses a popular model like FICO, different scoring models can weigh factors differently, leading to different scores even with the same data.

Is Experian Safe to Use? What Gen Z Should Know?

In 2014, Experian, alongside Equifax and TransUnion, became regulated by the Financial Conduct Authority. This means it has to comply with certain standards, offering consumers protection.

That said, it received an enforcement notice from the Information Commissioner’s Office (ICO) about the way it has “used personal data within their data broking businesses for direct marketing purposes”. The ICO has ordered it to make changes to “invisible” processing, where individuals are not aware “the organisation is collecting and using their personal data”. Experian is appealing against the ICO ruling.

Is Experian Safe to Use for Credit Reports and Scores?

The short answer: yes, Experian is generally safe—but you still need to stay alert.

Here’s what Experian does to protect your data:

- 🔐 Encryption: Your info is encrypted end-to-end.

- 🧑⚖️ Compliance: They’re regulated by federal laws like the Fair Credit Reporting Act (FCRA).

- 🔎 Monitoring: They offer fraud alerts and identity protection features (some free, some paid).

Is it 100% risk-free? No. No system is. But Experian is a legit financial institution that’s been around for decades. The real question is how you use it.

Is It Safe to Use Experian for a Credit Report?

If you’re just trying to see what’s on your credit file, you’re not exposing anything new—Experian already has that info. You’re just viewing it. Think of it like checking your attendance record in school—you’re not submitting anything, you’re just seeing what’s on file.

Just make sure you’re on the real Experian site or app (watch out for fake phishing links) and not sharing your login info.

Is It Safe to Use Experian Credit Score?

Yes—and checking it doesn’t lower your score. You’re performing what’s called a soft inquiry. This is completely safe and has no effect on your credit score. It’s different from a hard inquiry, which happens when you apply for a loan or credit card and a lender checks your credit report. Those can knock your score down a few points temporarily.

So if you’re just reviewing your score for your own awareness, it’s totally fine to check as often as you want.

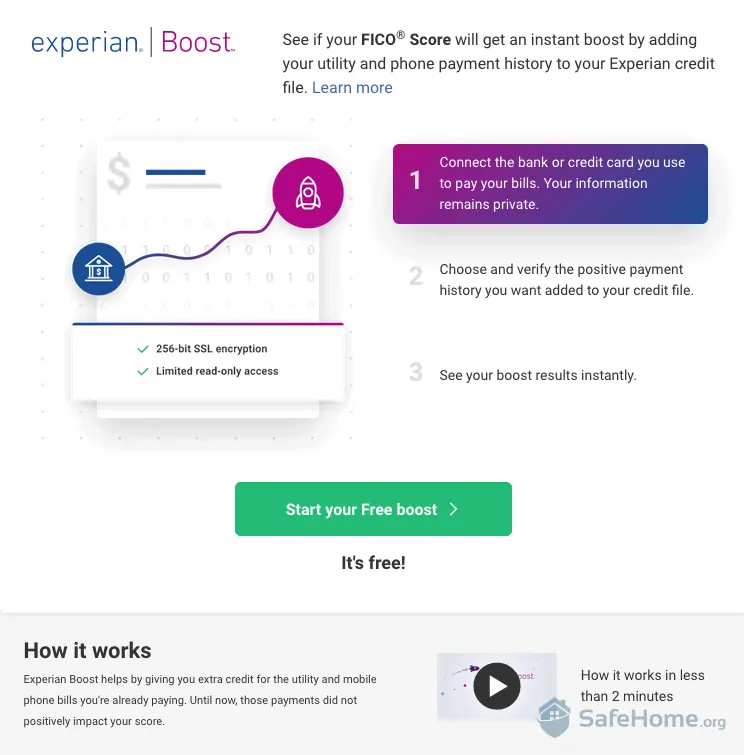

Is Experian Boost Safe to Use?

Experian Boost lets you link your bank account and earn credit for paying your bills—like your phone plan or Netflix—on time. It’s especially helpful if you’re just starting out and don’t have a traditional credit card or loan yet.

So, is it worth it?

- They use encrypted, bank-level security.

- It’s read-only access, meaning they can view your transactions but can’t move money.

- You can disconnect your account anytime.

That said, if you’re super protective about who sees your bank info, you might not love the idea. But if you’re struggling to build credit, it’s a legit shortcut—and far safer than predatory lending or endless denials.

If Boost feels like too much, there’s another solid option: you could opt for a secured credit card to build credit, like Step. These work by using your own money as a deposit, so you’re not borrowing from a bank—you’re basically building credit by spending your own money, safely. And because secured cards report to the credit bureaus, they can help you grow your score over time, just like a regular credit card. It’s a low-risk way to get started without linking your bank or relying on someone else’s approval.

Is Experian Really Free? What You’re Signing Up For

Yes, but with limits.

You can:

- Check your credit report and score for free

- Get some basic credit alerts

- Use Experian Boost at no cost

But there are premium features like identity theft protection, daily score updates, and advanced monitoring that cost extra. Just avoid accidentally enrolling in a free trial if you don’t want surprise charges.

How Your Experian Credit Report Helps You (or Not)

Your credit report isn’t just a number—it’s a detailed timeline of how you’ve handled money. Knowing what’s in it can help you:

- Catch fraud

- Fix errors that are hurting your score

- Understand what lenders see before you apply

What’s Actually on an Experian Credit Report?

- Your name, address, and employer history

- Credit cards and loans (open and closed)

- Missed or late payments

- Public records like bankruptcies

- Credit inquiries from lenders

It’s smart to review this regularly—especially before applying for something like an apartment or car loan.

FAQs About Experian

Does checking your score with Experian lower it?

Nope. That’s a soft inquiry—it doesn’t affect your score.

What is Experian’s credit score range?

Typically 300–850. A good score starts around 670.

Does your income affect your credit score?

No. Lenders care about income, but credit bureaus don’t track it.

Still figuring out what does affect your score? Read this: understanding credit scores

Alternatives to Experian for First-Time Credit Builders

If Experian feels a little too complex, there are beginner-friendly options like Step.

Step is a credit building app designed for people 13+. There’s no credit check to sign up, and it helps you build credit with everyday purchases—like food, rides, or bills—through a secured card that reports to major credit bureaus.

It’s simple, transparent, and designed specifically for people figuring credit out for the first time.

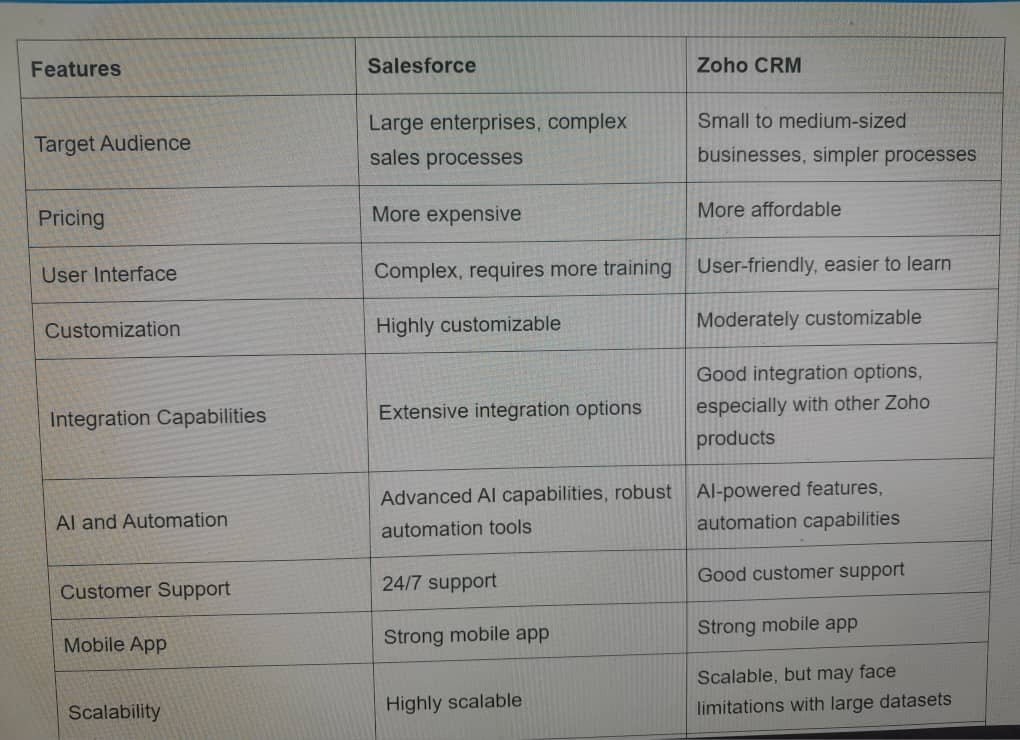

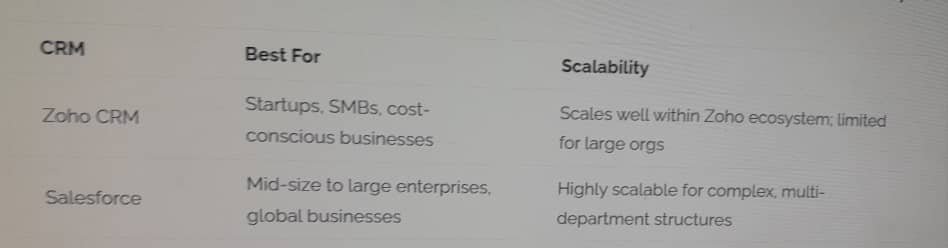

Salesforce vs Zoho: The Complete 2025 CRM Comparison Guide

Salesforce vs Zoho: The Trending rivalry between top B2B CRM providers remains a major concern for sales leaders

Table of Contents

- 1. Salesforce vs Zoho CRM overview

- 2. Salesforce vs Zoho CRM overview

- What Makes a Good CRM in 2025?

- Salesforce vs Zoho CRM- Features Comparison

- Salesforce Overview

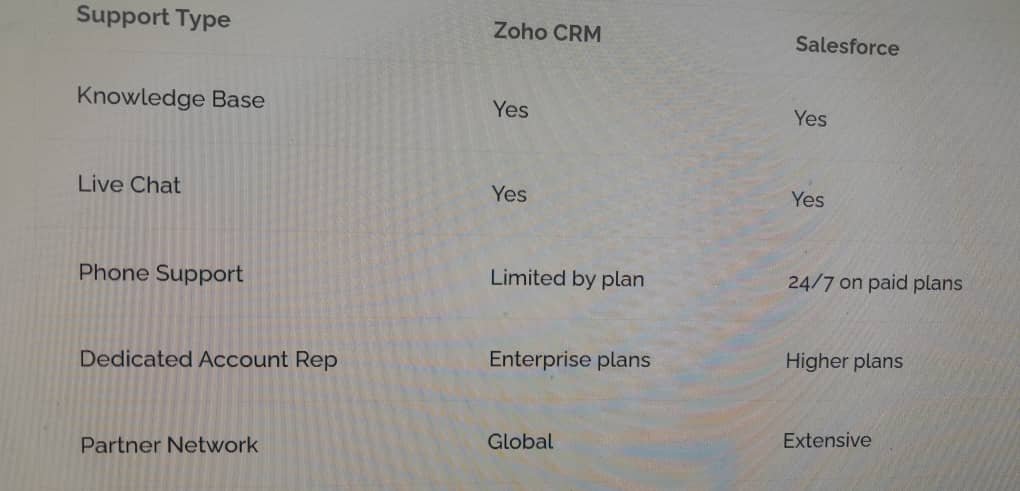

- Salesforce vs Zoho CRM-Customer Support Comparison

- Zoho CRM Overview

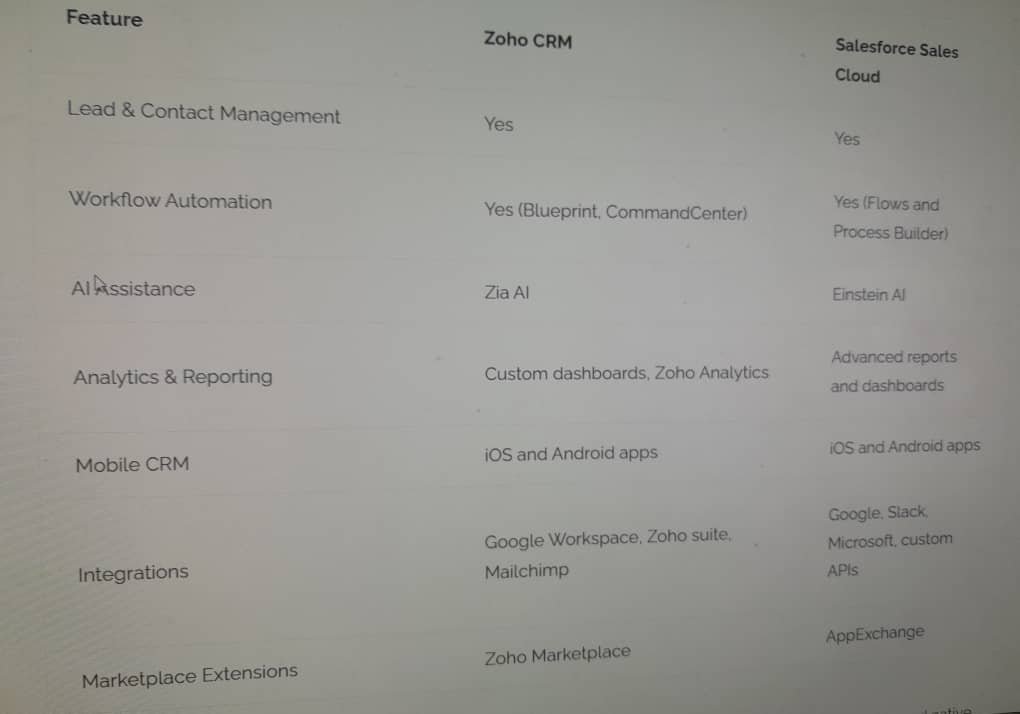

- Salesforce vs Zoho Features-by-Feature Breakdown

- Salesforce vs Zoho- Scalability Comparison

- Conclusion

- FAQs ; Salesforce vs Zoho

With the business environment more competitive now than ever before, businesses need all the possible advantages they can get, One of the main ways to gain this competitive advantage is by making your business processes more efficient through the use of a CRM.

So Choosing the right CRM can feel like standing at a crossroads even business owners and marketers face the same dilemma indeed there’s Salesforce, a giant trusted by enterprises around the world, On the other, Zoho CRM, a flexible and affordable solution loved by growing businesses.

It’s a tough choice oicking decision and if you’re here, you’re probably asking yourself the same question many business owners/marketers do: Which one actually fits my team, budget, and goals?

In this Salesforce vs Zoho comparison, we’ll unpack everything you need to know like updated trending pricing, usability, integrations, automation, and real-world advantages,inthe end, you’ll be ready to make a confident, no-hesistating decision so keep reading to get a full breakdown on which CRM is the best for your organization.

1. Salesforce vs Zoho CRM overview

| 💼 Category | 🚀 Salesforce | 🌿 Zoho CRM |

|---|---|---|

| 💰 Pricing | Starts at $25/user/month Advanced plans available 💎 👉 Explore |

Starts at $14/user/month Budget friendly for SMBs 🌱 👉 Explore |

| ⚙️ Features | Advanced automation, AI (Einstein), deep integrations, customizable workflows, strong analytics. | Easy setup, Zia AI (basic), strong mobile app, solid integrations, clean interface. |

| 📈 Scalability | Highly scalable — best for medium to large enterprises 🏢 | Great for small to medium businesses 🧩 |

| ✅ Pros |

|

|

| ❌ Cons |

|

|

| 🧰 Customer Support | 24/7 support, large knowledge base, Trailhead training platform 📞 | Email & chat support, solid knowledge base, priority support in higher plans 💬 |

| ✨ Additional Points | Best for businesses that want deep customization and robust reporting. Ideal for scaling teams 🚀 | Perfect for SMBs that want simplicity, speed, and affordability without complexity 🌱 |

2. Salesforce vs Zoho CRM overview

What Makes a Good CRM in 2025?

Before we dive into the head-to-head, let’s set the stage, A modern CRM isn’t just about storing contacts anymore, It’s your growth engine — the system that helps your team work smarter, close more deals, and stay organized.

So a solid CRM should deliver:

Clear, customizable dashboards

Smart automation that saves time

Seamless integrations with your favorite tools

Scalability to grow with your business

Reliable support when things get tricky

Both Salesforce and Zoho claim most of these boxes, but how well they do it can make a big difference.

Salesforce vs Zoho CRM- Features Comparison

Salesforce Overview

What Is Salesforce?

Salesforce is a heavyweight in the CRM space. It’s known for its enterprise-grade tools, impressive automation, and deep customization options. If you want a system that can grow as fast as your business, Salesforce is hard to beat.

Why businesses love it:

- Powerful sales and marketing automation

- Advanced forecasting and analytics

- Einstein AI for data-driven decisions

- Huge marketplace for integrations

The trade-off? It can feel a bit overwhelming for smaller teams, especially if you don’t have technical support on hand.

Salesforce vs Zoho CRM-Customer Support Comparison

Zoho CRM Overview

Zoho CRM is often described as “powerful without the pain.” It’s clean, affordable, and quick to set up making it a favorite for small and medium-sized businesses.

It Got Great Features Like ;

- Simple and intuitive design

- Budget-friendly pricing plans

- A complete ecosystem of Zoho apps

- Mobile-friendly tools for teams on the go

It might not have the sheer muscle of Salesforce, but for many businesses, it strikes the perfect balance between features and cost.

Salesforce vs Zoho Features-by-Feature Breakdown

- Ease of Use

Salesforce: Incredibly powerful but can take time to master. Larger teams often invest in onboarding or admin support.

Zoho CRM: Easy to navigate and beginner-friendly. Most teams can get started with little to no training.

- Pricing & Plans

Salesforce: Starts at $25 per user/month. Pricing can rise quickly as you add more advanced features.

Zoho CRM: Starts at $14 per user/month. More budget-friendly, especially for smaller teams.

- Automation & AI

Salesforce: One of the best in the industry for automation and AI forecasting.

Zoho CRM: Great automation for the price, though its AI features are more basic.

- Integrations & Ecosystem

Salesforce: Connects with thousands of apps, from marketing tools to ERP systems.

Zoho CRM: Works seamlessly with other Zoho products and popular third-party apps.

- Customization & Flexibility

Salesforce: Extremely flexible, but complex setups often need developers.

Zoho CRM: Offers enough customization for most SMBs — no coding skills required.

- Customer Support

Salesforce: 24/7 support plus access to Trailhead, its free learning platform.

Zoho CRM: Helpful support and a solid knowledge base. Priority support comes at a higher tier.

- Reporting & Analytics

Salesforce: Exceptional reporting features, great for sales forecasting.

Zoho CRM: Strong analytics for SMBs, but not as deep for enterprise use.

Pros and Cons of Salesforce & Zoho CRM

Salesforce Pros ✅

- Best-in-class automation and integrations

- Extremely customizable

- Trusted by large enterprises

- Great analytics and AI support

Salesforce Cons ❌

- Higher learning curve

- Price climbs fast as you scale

- May need admin or dev support

Zoho CRM Pros ✅

- Budget-friendly and easy to use

- Fast onboarding

- Great for small to midsize teams

- Strong mobile functionality

Zoho CRM Cons ❌

- Fewer advanced AI options

- Limited customization for complex setups

- Slower support on lower plans

- Which CRM Should You Choose?

If you’re running a smaller team or just starting out, Zoho CRM is a smart, budget-friendly pick that won’t bog you down with complexity.

If, however, your business is scaling fast, needs deep customization, or manages complex sales pipelines, Salesforce offers the power and flexibility to keep up.

Quick Recap:

- Choose Zoho CRM if you want ease of use and lower costs.

- Choose Salesforce if you need advanced features and don’t mind a learning curve.

Salesforce vs Zoho- Scalability Comparison

Conclusion

Both platforms(Salesforce vs Zoho) bring a lot to the table, it’s not about which one is “better” overall but which one is better for you.

Zoho CRM is perfect for teams who want to move fast without overspending. Salesforce shines for businesses ready to invest in a platform that can grow with them.

Don’t just rely on reviews. Sign up for their free trials and see which one actually fits your workflow.

FAQs ; Salesforce vs Zoho

- Is Zoho CRM cheaper than Salesforce?

Yes. Zoho CRM starts at $14/user/month, while Salesforce starts at $25/user/month. It’s more cost-effective for small teams.

- Which CRM is easier to learn?

Zoho CRM is generally easier thanks to its clean interface. Salesforce offers more features but requires more training.

- Can Zoho CRM work for larger businesses?

It can — though its sweet spot is small to mid-sized companies. For larger enterprises, Salesforce is often a better fit.

- Who has better AI?

Salesforce’s Einstein AI is more advanced, while Zoho’s Zia AI covers basic automation and insights.

- Do both offer free trials?

Yes. Both platforms let you try their tools before you commit.

External Sources

Salesforce Official Website

Zoho CRM Official Website

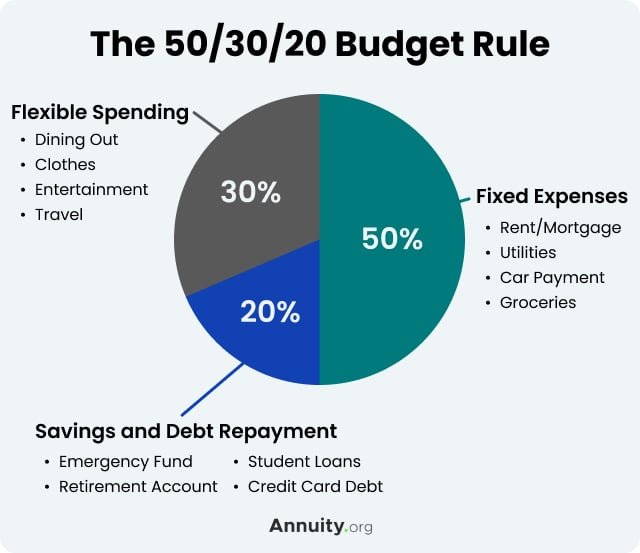

The 50/30/20 Rule of Budgeting & saving 2025: Best Monthly Budget Guide

Table of Contents

Most people save too little, and unknowingly spend too much. The 50/30/20 Rule of Budgeting & saving 2025 for budgeting is a way to become more aware of your financial habits and limit overspending and under-saving (by spending less on the things that don’t matter to you, you can save more for the things that do).

Because this is just a rule of thumb for planning your budget you’ll also need to supplement it with a system to monitor spending.

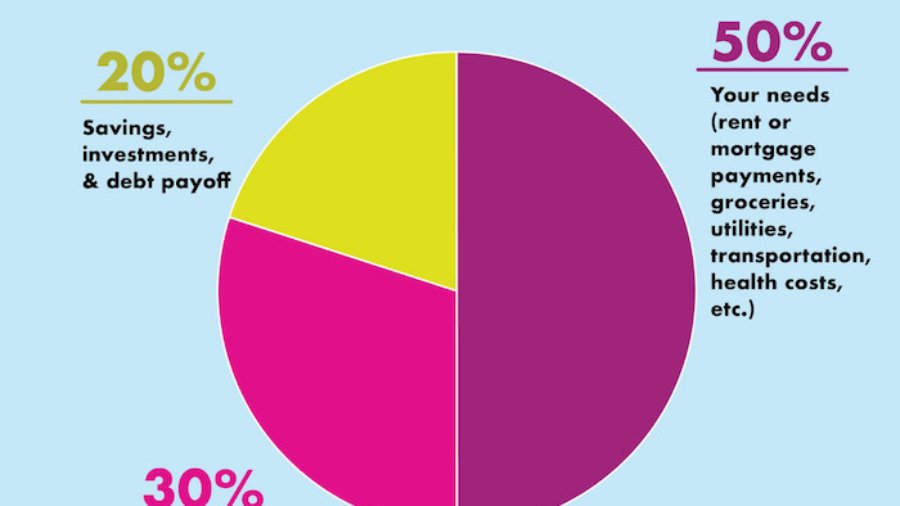

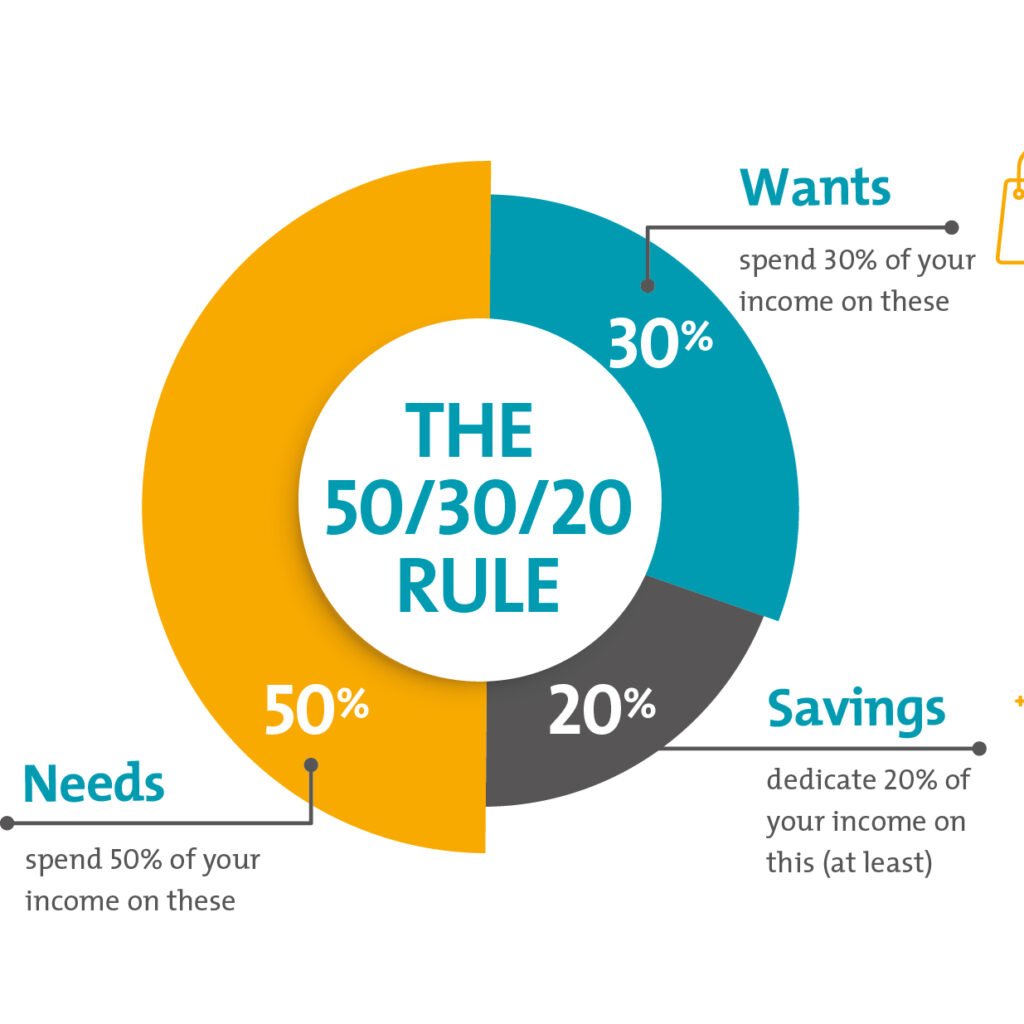

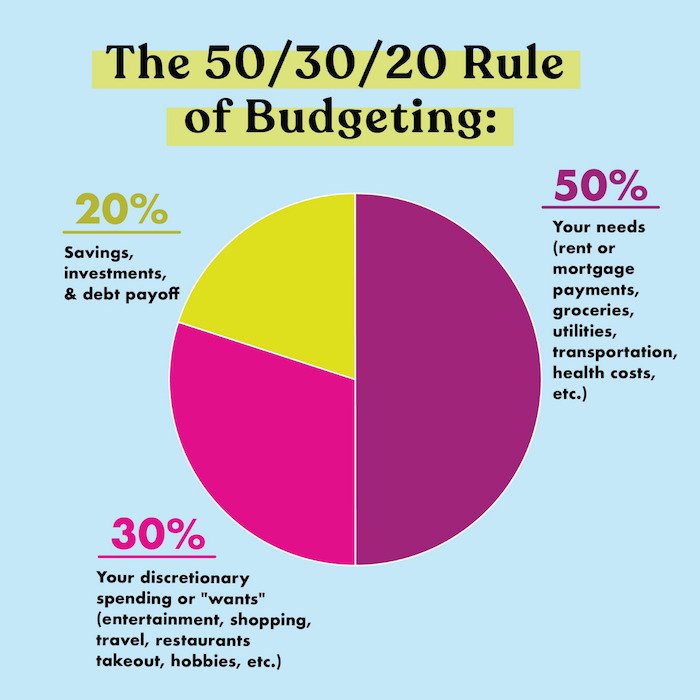

What is the The 50/30/20 Rule of Budgeting & saving 2025?

The 50/30/20 Rule of Budgeting & saving 2025 is a guideline for allocating your budget to three categories, ‘needs’, ‘wants’ and financial goals as follows:

50% to Needs

Needs are what you can’t live without, or at least very easily. They include things like:

- Rent/Mortgage payments

- Groceries

- Utilities, such as electricity and water

30% to Wants

Wants are things that you desire but don’t actually need to survive. They might include:

- Hobbies

- Holidays

- Dining out

- Digital and streaming services like Netflix and Amazon.

20% to Financial Goals

This category includes savings and money set aside for debt payments.

How to use The 50/30/20 Rule of Budgeting & saving 2025

- Calculate your monthly income. Add up how much guaranteed income you receive in your bank account each month.

- Calculate a spending threshold for each category: Multiply your take-home pay by 0.50 (for needs), 0.30 (for wants), and 0.20 (for financial goals) to see how much you should ideally spend in each category.

- Plan your budget around these numbers: Think of these three categories as “buckets” that you can fill with monthly expenses. List and tally your monthly expenses under the category each falls into and see if you’re spending less than the monthly targets you established in the prior step.

- Follow your budget: Track your expenses each month, and make changes where needed, in order to stick to your spending thresholds going forward

The 50/30/20 Rule of Budgeting & saving 2025 vs. Other Budgeting Methods

The 50/30/20 Rule of Budgeting & saving 2025 of thumb isn’t the only game in town. Here are a few other budgeting techniques to consider:

80/20 Rule: With this method, you immediately set aside 20% of your income into savings. The other 80% is yours to spend on whatever you want, no tracking involved.

Advantages of The 50/30/20 Rule of Budgeting & saving 2025

Simplicity: Its greatest strength is its simplicity. It’s easy to understand and implement, making it perfect for budgeting beginners who are intimidated by more granular methods.

Flexibility: The rule uses broad categories, which gives you flexibility in your spending. You don’t have to track every single penny in dozens of subcategories. As long as you stay within your three main buckets, you’re on track.

Promotes Balanced Financial Health: It forces you to prioritize savings and debt repayment by dedicating a significant 20% of your income to these goals. At the same time, it builds in a 30% allowance for “wants,” preventing the burnout that can come from overly restrictive budgets.

Disadvantages of The 50/30/20 Rule of Budgeting & saving 2025

Challenging in High Cost of Living (HCOL) Areas: In expensive cities, housing and other “needs” can easily consume more than 50% of income, making the rule difficult to follow without significant sacrifices.

Not Ideal for Irregular Income: For freelancers or those with variable paychecks, basing the percentages on a fluctuating income can be challenging.

May Not Be Aggressive Enough for High Debt: If you have substantial high-interest debt, the 20% allocation might not be aggressive enough. In this case, a more debt-focused approach may be necessary.

Compared to a method like zero-based budgeting, where every single dollar is assigned a “job,” the 50/30/20 rule is less rigid. Zero-based budgeting offers more control and precision but requires significantly more time and effort to maintain. For many, the 50/30/20 rule provides a “good enough” structure that is easier to stick with long-term.

How to Apply The 50/30/20 Rule of Budgeting & saving 2025 With Low Income

A common criticism of this rule is that it doesn’t work for everyone, especially those with lower incomes. Learning how to apply 50/30/20 with low income requires creativity and flexibility, but it can still be a valuable guideline.

The key is to treat the percentages as a goal, not a strict law.

Adjust the Percentages: If your needs exceed 50%, don’t give up. You might need to adjust to a 60/20/20 or even a 70/15/15 split temporarily. The priority is to cover your needs first, then ensure you are still saving something—even a small amount—before allocating to wants.

Focus on Cutting “Wants” First: When money is tight, the “wants” category is the first place to look for cuts. This could mean canceling subscriptions, cooking at home more often, or finding free entertainment options.

Protect Your Savings Goal: Even if you can only save 5% or 10% of your income, make it a priority. Paying yourself first, no matter how small the amount, builds a crucial financial habit. Automate this transfer on payday so you aren’t tempted to spend it.

Case Study Example:

Maria earns $2,200 per month after taxes. A strict 50/30/20 split would be $1,100 (Needs), $660 (Wants), and $440 (Savings). However, her rent and utilities alone cost $1,200.

Instead of abandoning budgeting, she adjusts. Her “Needs” are closer to 60% ($1,320). She decides to keep her savings goal at 20% ($440) as she wants to build an emergency fund. This leaves her with 20% ($440) for “Wants” and all other variable expenses for the month. It’s tight, but by focusing on free social activities and cooking at home, she makes it work.

Alternatives to the 50/30/20 Rule

If the 50/30/20 framework doesn’t feel right for you, don’t worry. There are many other effective budgeting methods. The best one is always the one you can stick with consistently. Here are a few popular alternatives to the 50/30/20 rule:

Zero-Based Budgeting: As mentioned, this method involves assigning a purpose to every single dollar you earn. Your income minus your expenses should equal zero at the end of the month. It’s perfect for meticulous planners who want maximum control over their money.

The Envelope Method: A classic cash-based system. You withdraw cash for your variable spending categories (like groceries, gas, entertainment) and put it into labeled envelopes. When the envelope is empty, you’re done spending in that category for the month. It’s highly effective for curbing overspending.

The 70/20/10 Rule: This is a variation often recommended for those who want to prioritize saving and investing more aggressively. It allocates 70% to spending (both needs and wants combined), 20% to savings, and 10% to debt repayment or investing.

You might choose an alternative if you have a very specific goal, such as rapid debt elimination, or if you find the broad categories of the 50/30/20 rule too vague.

Practical Tips to Stick With the Rule

Creating a budget is one thing; sticking to it is another. Here are some tips to help you stay on track.

Automate Your Savings: This is the most powerful trick in the book. Set up an automatic transfer from your checking account to your savings or investment account every payday. This “pays yourself first” and ensures your 20% goal is met without relying on willpower.

Use Apps to Track Your Expenses: Use a budgeting app (like Mint, YNAB, or your bank’s built-in tools) to automatically categorize your spending. This makes it easy to see where your money is going and whether you’re staying within your 50/30/20 targets.

Review and Adjust Monthly: Your budget isn’t set in stone. Life happens. A car repair or an unexpected bill can throw things off. Review your spending at the end of each month. See what worked and what didn’t, and adjust your plan for the next month accordingly.

FAQs Of The 50/30/20 Rule of Budgeting & saving 2025

What is the 50/30/20 budget rule in simple terms?

In simple terms, it’s a rule of thumb for managing your money. You divide your after-tax income into three parts: 50% for essential needs (like rent and groceries), 30% for non-essential wants (like hobbies and dining out), and 20% for savings and paying off debt.

Is the 50/30/20 budget realistic?

For many people, yes, it is very realistic because of its simplicity and flexibility. However, it can be unrealistic for those in very high cost-of-living areas or for individuals with very low incomes or extremely high debt, as their “needs” may take up a much larger portion of their income.

Can I use the 50/30/20 rule with debt?

Absolutely. The “20%” category is explicitly for Savings and Debt Repayment. If you have high-interest debt, like from credit cards, you should prioritize paying it down within this 20% category. Once your high-interest debt is gone, that entire 20% can be shifted toward savings and investing.

What is better than the 50/30/20 rule?

There is no single “better” budget; the best budget is personal. A zero-based budget might be better for someone who needs strict control over every dollar. The envelope system might be better for someone who struggles with overspending on debit or credit cards. The 50/30/20 rule is often best for beginners who need a simple, balanced starting point.

Conclusion

Mastering your money doesn’t have to be complicated. The 50/30/20 budget rule offers a powerful, accessible, and balanced approach to financial management. By dividing your income into Needs, Wants, and Savings, you create a clear roadmap for your spending that aligns with your financial goals. It provides structure without being overly restrictive, empowering you to cover your bills, enjoy your life, and still build a strong financial foundation for the future.

While it may not be the perfect fit for every single person, it serves as an excellent starting point. Give it a try for a month or two. Track your spending, see how it aligns with the 50/30/20 ratios, and make adjustments as needed. You might find that it’s the simple framework you’ve been looking for to finally achieve financial peace of mind.

Top 5 Best Robo-Advisors of 2025 for Hands-Off Investing

Table of Contents

Introduction

Top 5 Best Robo-Advisors of 2025

Does the thought of picking individual stocks, analyzing market trends, and constantly checking your portfolio sound more like a chore than an opportunity? You’re not alone.

The world of investing can feel overwhelmingly complex, but what if you could put your financial growth on autopilot, guided by technology designed to make smart decisions for you?

Welcome to the world of robo-advisors. These digital platforms have revolutionized investing, making it accessible, affordable, and stress-free for millions. Whether you’re a complete beginner or a seasoned investor looking for a passive strategy, the right robo-advisor can be a game-changer for reaching your financial goals.

In this comprehensive guide, we’re cutting through the noise to bring you the definitive list of the top 5 Best robo-advisors in 2025 ,for beginners and passive investors. We’ll break down their fees, features, and unique strengths to help you choose the perfect partner for your hands-off investing journey.

What Exactly Is a Robo-Advisor (and Why Should You Care)?

Before we dive into our top(Top 5 Best Robo-Advisors of 2025) picks, let’s quickly clarify what a robo-advisor is. Think of it as a digital financial advisor. Instead of meeting with a person, you use a sophisticated computer algorithm to manage your investment portfolio.

Here’s how it typically works:

- You answer a questionnaire: You’ll provide information about your financial goals (like saving for retirement or a down payment), your timeline, and your comfort level with risk.

- The algorithm builds a portfolio: Based on your answers, the robo-advisor creates a diversified portfolio for you, usually using low-cost exchange-traded funds (ETFs).

- It manages everything automatically: The platform will automatically rebalance your portfolio to keep it aligned with your goals and can even perform advanced strategies like tax-loss harvesting to save you money.

The primary benefit is simplicity. For a small annual fee, you get a professionally managed portfolio without needing any prior investing experience. This makes them one of the best tools for passive investors who want to build wealth over the long term.

How We Chose the Top Robo-Advisors for 2025

To identify the best of the best, we evaluated each platform based on a set of crucial criteria tailored for beginners and hands-off investors, solely sticked to the current tittle(Top 5 Best Robo-Advisors of 2025)

Our ranking considers:

- Management Fees: How much does it cost to use the service? Lower fees mean more of your money stays invested and working for you.

- Minimum Investment: How much money do you need to get started? We prioritized platforms with low or no minimums.

- Key Features: Does the platform offer valuable tools like automatic rebalancing, tax-loss harvesting, and goal-based planning?

- Human Advisor Access: For those who want the option of talking to a real person, we looked for hybrid models that offer access to financial planners.

- User Experience: Is the platform easy to navigate on both desktop and mobile? A clean interface is essential for a stress-free experience.

A Deep Dive: The Top 5 Best Robo-Advisors of 2025

After extensive research, here are our picks for the top 5 Best robo-advisors in 2025 for beginners and passive investors. Each one excels in a specific area, ensuring there’s a perfect fit for your needs.

1. Betterment

Betterment has long been a leader in the Top 5 Best robo-advisors of 2025, and for good reason. Its platform is incredibly intuitive, built around helping you set and achieve specific financial goals. Whether you’re saving for retirement, a new home, or simply building wealth, Betterment creates a tailored plan for each objective.

Key Features:

- Management Fee: 0.25% annually for the Digital plan.

- Minimum Investment: $0 to get started ($10 to start investing).

- Best For: Beginners who want a simple, goal-oriented approach to investing.

- Standout Feature: Excellent goal-planning tools and a feature called “Tax-Coordinated Portfolio” that strategically places assets across different account types to reduce your tax burden.

For a slightly higher fee (0.40%), Betterment’s Premium plan provides unlimited access to Certified Financial Planners (CFPs), making it a fantastic hybrid option as your assets grow.

2. Wealthfront

Wealthfront is another pioneer in automated investing and is a top contender, especially for those with taxable investment accounts. Its software-first approach delivers one of the most robust tax-loss harvesting services on the market, available to all clients regardless of account balance.

Key Features:

- Management Fee: 0.25% annually.

- Minimum Investment: $500.

- Best For: Investors with taxable accounts who want to maximize their tax savings.

- Standout Feature: “PassivePlus®” suite of features, which includes industry-leading tax-loss harvesting, stock-level tax-loss harvesting for larger accounts, and risk parity strategies.

While it doesn’t offer dedicated human advisors, its digital financial planning tools are exceptionally detailed, allowing you to model complex scenarios like buying a house or taking time off to travel.

3. SoFi Invest Automated Investing

SoFi has built a massive financial ecosystem, and its Automated Investing platform is a core part of it. The biggest draw? It’s completely free. SoFi charges no advisory fees for its robo-advisor service, making it an unbeatable choice for cost-conscious investors.

Key Features:

- Management Fee: $0.

- Minimum Investment: $1.

- Best For: Beginners and existing SoFi members who want zero management fees.

- Standout Feature: Access to human financial advisors at no extra cost. Plus, being a SoFi member unlocks discounts on other SoFi products like loans and banking.

The trade-off for the free service is the lack of tax-loss harvesting. However, for those investing primarily in retirement accounts like a Roth IRA, this feature isn’t necessary, making SoFi an incredibly compelling option.

4. Schwab Intelligent Portfolios – Best for Large Balances and No Advisory Fees

Charles Schwab, a titan in the traditional brokerage world, offers a powerful robo-advisor with its Intelligent Portfolios platform. Similar to SoFi, it charges no advisory fees. However, it requires a higher minimum investment, positioning it for investors who are starting with a bit more capital.

Key Features:

- Management Fee: $0 (though a portion of your portfolio is held in cash, which earns interest for Schwab).

- Minimum Investment: $5,000.

- Best For: Investors with at least $5,000 who want a sophisticated portfolio from a trusted brand without paying advisory fees.

- Standout Feature: Portfolios are constructed from over 50 different ETFs, offering deep diversification. Tax-loss harvesting is available for accounts with $50,000 or more.

For those with over $25,000, Schwab offers a Premium tier that includes unlimited guidance from a CFP for a one-time planning fee and a small monthly subscription, providing an excellent hybrid model.

5. Fidelity Go