Introduction: Ready to Boost Your Credit Score Fast?

Have you ever checked your credit score and felt that sinking feeling—it’s lower than you thought? You’re not alone. Whether you’re planning to buy a home, get a car loan, or simply qualify for better credit card rates, improving your credit score can make all the difference.

The good outcomes is You can raise your credit score fast—sometimes even Boost your credit score in 30 days—by following the right strategies. In this post, we’ll uncover 10 proven ways to give your score a serious boost and get you closer to financial freedom.

check your credit status/Report with FREE legit tools verified by international credit Bureaus:

Request your report from Equifax, Experian, and TransUnion.

Review all accounts for errors, late payments, or unknown inquiries.

By understanding your report, you can take targeted steps to raise your credit score fast and fix mistakes that may drag it down.

3: Dispute Errors: Step-by-Step Process + Free Template

Errors happen more often than you think.

A single mistake could lower your score by 50+ points! if the following steps didnt solve your issue contact us here with Free help.

Here’s how to fix it:

Step-by-Step to Dispute Errors

Identify the incorrect entry on your credit report.

Gather proof (bank statements, receipts, etc.).

Submit a dispute directly with the credit bureau online.

Free Email Template:

Subject: Request to Remove Incorrect Entry from My Credit Report

Dear [Credit Bureau], I recently reviewed my credit report and found an inaccurate item: [describe issue]. Please investigate and remove this error. Attached are supporting documents.

Thank you, [Your Full Name] [Your Address] [Last Four Digits of your SSN]

Disputing incorrect items can significantly increase your credit score in 30 days once corrected.

Use a credit monitoring tool (like Experian, Credit Karma, or SmartCredit) to track your score weekly. Monitoring helps you spot issues early and celebrate your progress.

Conclusion: Your 30-Day Path to a Better Credit Score

Raising your credit score doesn’t have to take years. By applying these 10 proven methods, you can increase your credit score in 30 days—or even sooner.

Remember, the key to success is consistency and awareness. Check your report, manage utilization, and use credit wisely. You’ll be surprised how fast results show up.

Start today and see how quickly you can raise your credit score fast toward your financial goals!

FAQs: Raise Credit Score Fast – Common Questions Answered

1. Can I really increase my credit score in 30 days?

Yes! Paying down balances, correcting report errors, and lowering utilization can show results within a single billing cycle.

2. What’s the fastest way to raise my credit score 100 points?

Combine multiple tactics: pay down debt, remove errors, and use credit-builder tools.

3. Does checking my credit score lower it?

No. Checking your own credit is a soft inquiry and doesn’t affect your score.

4. How often should I check my credit report?

Review it every month, especially if you’re trying to raise your credit score fast.

5. Are credit repair companies worth it?

They can help, but you can often do the same steps yourself for free using the methods above.

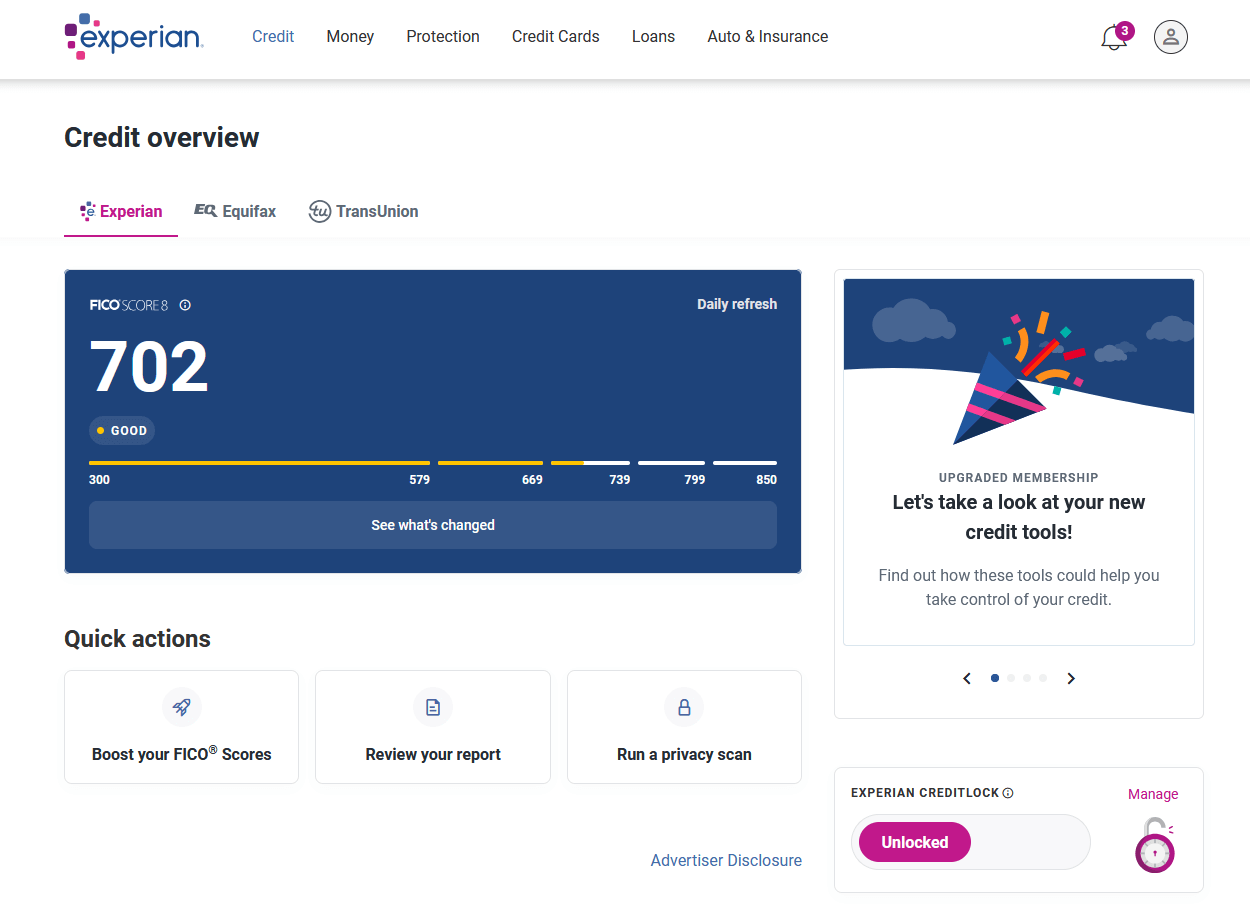

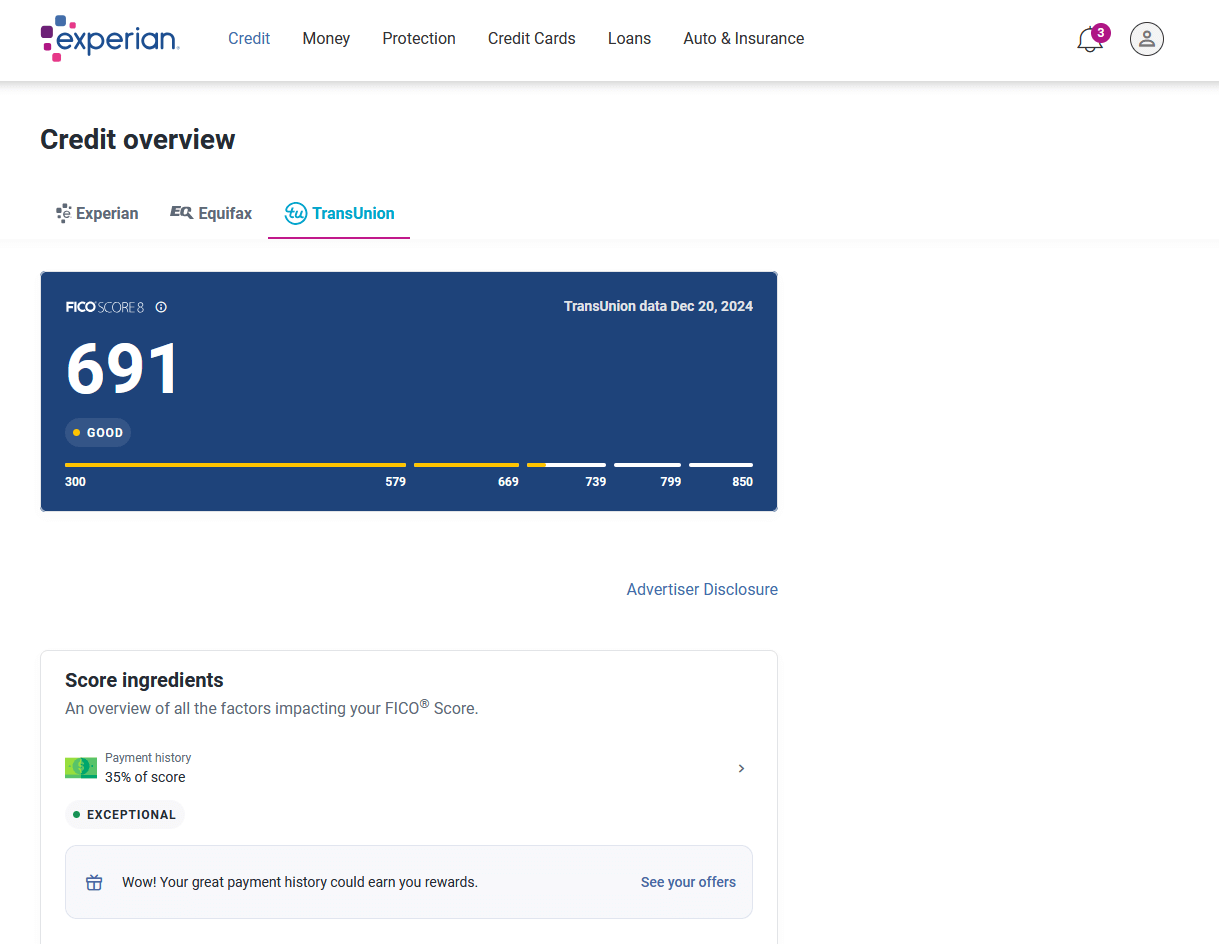

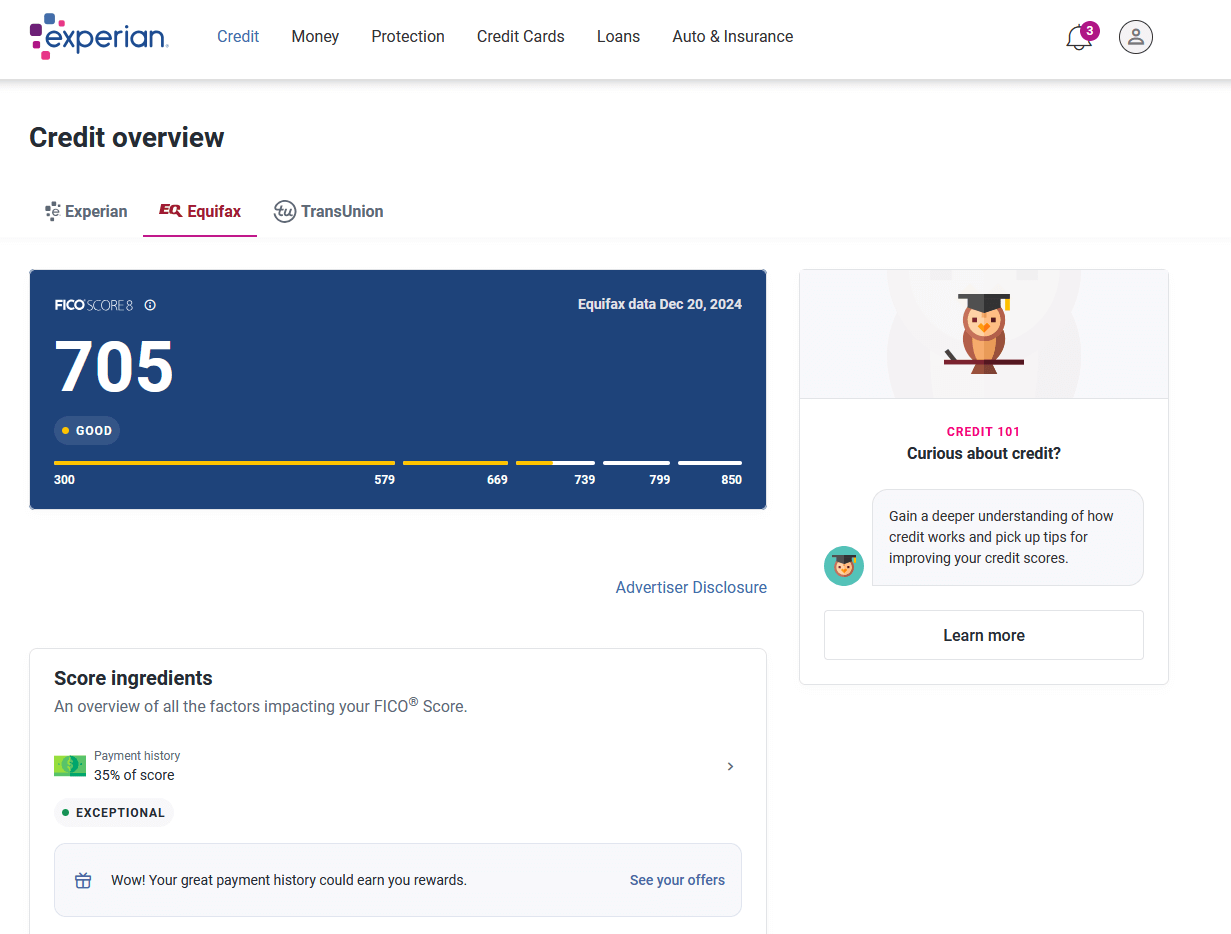

Experian review 2025| What is Experian what does Experian do?

our Guide today(Experian review 2025) focus one of the leading in credit business and activities,Experian is one of the three major credit bureaus in the US, alongside TransUnion and Equifax, It offers credit monitoring, score tracking, and identity protection services with different levels of coverage we will explain bit by bit our trending topic Experian review 2025.

Experian is a global data and technology company, powering opportunities for people and businesses around the world, by helping to redefine lending practices, uncover and prevent fraud, simplify healthcare, deliver digital marketing solutions, and gain deeper insights into the automotive market, all using unique combination of data, analytics and software.

They also assist millions of people to realize their financial goals and help them to save time and money.

We operate across a range of markets, from financial services to healthcare, automotive, agrifinance, insurance, and many more industry segments.

I’ve thoroughly examined Experian’s identity protection products with our research team, Apart from being one of the three primary credit bureaus, Experian has become a significant player in the identity protection industry with its IdentityWorks platform.

In this review(Experian review 2025), I will examine Experian’s credit monitoring services, security protocols, and security features. In order to assist you in determining whether its services are cost-effective and whether recent security incidents should sway your decision, I will carry out extensive testing and analysis.

🌟 Experian Overview

⭐ Rating: 4.5 / 5

💰 Price: $24.99/ month

✅ Free Version: Yes with no limits

📱 Platforms: Web, iOS, Android

🔔 Credit Monitoring: Included

🛡️ Insurance: 1$ million +Identity theft insurance

✨ Additional Features: Credit score simulation, alerts, and reporting tools,social security number monitoring

IdentityWorks is now a closed service that can only be accessed with a complementary code. Meanwhile, the IdentityWorks technology appears to have been migrated into the CreditWorks dashboard. So, the normal CreditWorks subscription now includes the full IdentityWorks identity protection technology. For accessibility, I will refer to IdentityWorks and CreditWorks interchangeably throughout this review.

Experian IdentityWorks features

During my testing, IdentityWorks and CreditWorks offered a rich set of features but a few notable limitations. Here’s a closer look at what the service provides:

Experian Identity Protection Features by Plan

Feature

Basic Plan

Premium Plan

Family Plan

Dark Web Monitoring

✔️

✔️

✔️

Real-Time Fraud Alerts

✔️

✔️

✔️

Credit Monitoring (1 Bureau)

✔️

✔️

✔️

Credit Monitoring (3 Bureaus)

❌

✔️

✔️

Identity Theft Insurance ($1M)

✔️

✔️

✔️

Social Security Number Monitoring

❌

✔️

✔️

Bank Account & Credit Card Monitoring

❌

✔️

✔️

Lost Wallet Assistance

❌

✔️

✔️

Child Identity Monitoring

❌

❌

✔️

Daily Credit Score Tracking

❌

✔️

✔️

Customer Support (24/7)

✔️

✔️

✔️

The old pricing model for IdentityWorks was simple: a free plan for basic Experian credit monitoring, a $24.99/month Premium plan for in-depth individual protection, and a $34.99/month Family plan, enough for two adults plus ten children. Each tier adds to features and levels of protection progressively, with paid plans providing critical services like three-bureau monitoring and identity theft insurance. Under the new, combined model, the Family subscription tier has disappeared, and there is only a CreditWorks Basic (free) and CreditWorks Premium option at $24.99/month.

Experian: Pros and Cons

✅ Pros

Free credit reports and scores available

Trusted by millions worldwide

Real-time credit alerts and monitoring

Identity theft protection options

User-friendly website and mobile app

❌ Cons

Some premium features require a subscription

Reports may contain outdated information

Customer service can be hard to reach

Data breaches have occurred in the past

Complex cancellation process for subscriptions

According to my testing, Experian’s biggest pros are its extensive monitoring and credit reporting. With a wide range of identity protection features – especially in paid plans – you can find coverage that suits your needs, including some features like court record monitoring and social network spying.

That said, users should be mindful of the operational challenges, including the complex interface and known customer service challenges. Although the recent platform improvements are promising, the expected premium charges have already raised questions regarding the system’s reliability and whether it might affect the overall user experience. It all boils down to whether you care more about complete monitoring than the interface is simple to use and customer support is a prompt response away.

Our methodology

A thorough review takes more than reading promotional materials or skimming other articles. Our specialists have developed and refined specific testing criteria to examine how Experian IdentityWorks performs in real-world conditions. We focus on five key components of identity theft protection, each weighted according to its importance in keeping you safe.

Protection features (30%). We rigorously test core monitoring capabilities, including three-bureau credit tracking, dark web surveillance, Social Security number monitoring, and financial account protection.

Monitoring and alerts (25%). Our team evaluates alert speed, accuracy, and customization options by tracking how quickly and reliably the service responds to potential threats.

Recovery services (20%). We assess the effectiveness of recovery specialists, examine insurance coverage details, and verify the quality of support for credit freezes and fraud resolution.

User experience (15%). We evaluate platform usability, mobile app functionality, and the accessibility of educational resources through hands-on testing.

Value for money (10%). We analyze pricing structures against feature sets and compare family plan options with competitor offerings to determine true market value.

How much does Experian cost?

Experian Pricing Features Comparison

Feature

Basic Plan

Premium Plan

Family Plan

Free Trial

Free forever (limited features)

7-day free trial for 1 user

7-day trial with child ID monitoring (up to 10 kids)

Monthly Subscription

Free

$24.99/month

$34.99/month

Annual Plan Option

❌

✅

✅

Cancel Anytime

✅

✅

✅

Family Coverage

❌

❌

✅ (up to 10 children)

Daily Credit Reports

❌

❌

✅

Daily FICO Score Updates

❌

✅

✅

Access to Tri-Bureau Credit Data

❌

✅

✅

Premium Support Access

❌

✅

✅

Lost Wallet Assistance

❌

✅

✅

These plans offer strong protection, but it’s important to add that competitors like Aura protect five adults and unlimited children for $30/month. For users prioritizing direct bureau integration and robust monitoring capabilities, Experian is worth the price.

key features of Experian review 2025:

Credit score monitoring: One of the things I liked most about Experian is the chance to get a free credit report. You can check it along with your FICO score without sharing your credit card details.

Credit reports: Experian also helps you keep track of your credit reports. You can opt for a free credit monitoring service, which gives you daily updates of any credit changes or score drops.

Dark web surveillance: Experian also comes with a great range of cybersecurity tools, including Dark Web monitoring, which actively looks for your personal information appearing on the Dark Web and sends real-time alerts. While comprehensive cybersecurity tools are available in paid plans, you can also do a quick Dark Web scan for free.

Credit locking and fraud resolution assistance: Unlike other bureaus, which only offer credit freezing (and it usually takes days to freeze/unfreeze), Experian came up with a neat CreditLock feature. It allows you to prevent unauthorized credit pulls and related activity. Furthermore, you can also set up fraud alerts and receive real-time notifications from a designated fraud resolution agent for further instructions. In worst-case scenarios, Experian keeps you covered with up to $1 million in identity theft insurance.

FICO score simulator: Instead of just checking your credit score, Experian also helps you run simulations to see how you might improve it. I especially liked playing with all the different options and checking how they would reflect on my credit score, and I find this feature to be useful for most consumers.

During my testing, IdentityWorks and CreditWorks offered a rich set of features but a few notable limitations. Here’s a closer look at what the service provides:

Experian Identity Protection Features by Plan

Feature

Basic Plan

Premium Plan

Family Plan

Dark Web Monitoring

✔️

✔️

✔️

Real-Time Fraud Alerts

✔️

✔️

✔️

Credit Monitoring (1 Bureau)

✔️

✔️

✔️

Credit Monitoring (3 Bureaus)

❌

✔️

✔️

Identity Theft Insurance ($1M)

✔️

✔️

✔️

Social Security Number Monitoring

❌

✔️

✔️

Bank Account & Credit Card Monitoring

❌

✔️

✔️

Lost Wallet Assistance

❌

✔️

✔️

Child Identity Monitoring

❌

❌

✔️

Daily Credit Score Tracking

❌

✔️

✔️

Customer Support (24/7)

✔️

✔️

✔️

Experian’s credit monitoring operates through daily scans rather than instant updates, checking for changes across credit files. Premium and Family plan members receive monitoring capabilities that cover all three credit bureaus, while the Basic plan monitors only Experian data. Daily credit reports and FICO scores – on paid plans only – help you track your credit health over time.

Premium plans give you access to reports from TransUnion.

And Equifax as well:

The identity protection suite includes dark web surveillance across 600,000 web pages, though users need to specify which information to monitor.

Experian IdentityWorks Identity Theft Protection Plans and Pricing for 2025

Experian Pricing Features Comparison

Feature

Basic Plan

Premium Plan

Family Plan

Free Trial

Free forever (limited features)

7-day free trial for 1 user

7-day trial with child ID monitoring (up to 10 kids)

Monthly Subscription

Free

$24.99/month

$34.99/month

Annual Plan Option

❌

✅

✅

Cancel Anytime

✅

✅

✅

Family Coverage

❌

❌

✅ (up to 10 children)

Daily Credit Reports

❌

❌

✅

Daily FICO Score Updates

❌

✅

✅

Access to Tri-Bureau Credit Data

❌

✅

✅

Premium Support Access

❌

✅

✅

Lost Wallet Assistance

❌

✅

✅

These plans offer strong protection, but it’s important to add that competitors like Aura protect five adults and unlimited children for $30/month. For users prioritizing direct bureau integration and robust monitoring capabilities, Experian is worth the price.

How does Experian work?

Experian collates information from a number of different sources, including:

Personal information, such as your date of birth, address and whether you are on the electoral roll. Existing credit agreements, including how much of your credit limit you are using (known as “credit utilisation”), your track record of making payments on time and any late or missed payments. Examples of problems with debt include defaults, CCJs, IVAs and bankruptcy. These only appear on your credit report for 6 years before being removed. Experian doesn’t include information about your employment, salary or income, or health expenses. It does, however, look at how often you apply for credit and whether you have been turned down for credit in the past.

It uses all of this information to come up with a score between 0-999, with 999 being the perfect score. This number gives lenders a guide to your potential creditworthiness, although different lenders will view your score differently rather than there being a one-size-fits-all approach. In short, viewing your Experian credit score, alongside your score with other credit reference agencies, will give you an indication of whether you are likely to be approved for credit, but it doesn’t act as a guarantee.

Experian review ? Free Credit Score Rating

Credit Score Rating Guide

Credit Score Range

Rating

What It Means

961 – 999

Excellent

You’re very likely to be approved for credit at the best rates.

881 – 960

Good

You should be eligible for most credit cards, loans, and mortgages.

721 – 880

Fair

You might get approved, but not at the best interest rates.

561 – 720

Poor

You may struggle to get credit and will likely pay higher rates.

0 – 560

Very Poor

You’re unlikely to be approved for most credit without improvement.

What is the most accurate credit score?

As with other credit reference agencies, Experian uses information collected from official sources and lenders. There is the potential for errors to occur or for out-of-date entries to drag your score down. Experian, Equifax and TransUnion also collect data from different sources, so your report will often vary significantly across all three, including the overall credit score you are given. It is, therefore, worth checking your report with all three providers, correcting any errors and making a note of the overall credit score for each. This is all the more important as you can’t be sure which of the providers’ reports lenders will use when you apply for products in the future. You could, for example, have checked your Experian score, but the lender refers to the Equifax report, which could have a different overall credit rating that makes you less likely to be accepted.

How to ensure accuracy

Dispute errors: If you find errors, file a dispute with the credit bureau to have the information corrected.

Check all three reports: You are entitled to a free credit report from each bureau (Experian, Equifax, and TransUnion) every 12 months at AnnualCreditReport.com.

Review for errors: As you check your reports, look for any inaccuracies, such as incorrect personal information, accounts that don’t belong to you, or wrong payment statuses.

Why Experian may differ from other Credit Agencies(Services)

Reporting schedules: Lenders do not report to all three bureaus at the exact same time, so credit reports can have different information at any given moment.

Data sources: Each bureau may receive information from a different set of creditors, leading to variations in the accounts listed on each report.

Scoring models: While Experian uses a popular model like FICO, different scoring models can weigh factors differently, leading to different scores even with the same data.

Is Experian Safe to Use? What Gen Z Should Know?

In 2014, Experian, alongside Equifax and TransUnion, became regulated by the Financial Conduct Authority. This means it has to comply with certain standards, offering consumers protection.

That said, it received an enforcement notice from the Information Commissioner’s Office (ICO) about the way it has “used personal data within their data broking businesses for direct marketing purposes”. The ICO has ordered it to make changes to “invisible” processing, where individuals are not aware “the organisation is collecting and using their personal data”. Experian is appealing against the ICO ruling.

Is Experian Safe to Use for Credit Reports and Scores?

The short answer: yes, Experian is generally safe—but you still need to stay alert.

Here’s what Experian does to protect your data:

🔐 Encryption: Your info is encrypted end-to-end.

🧑⚖️ Compliance: They’re regulated by federal laws like the Fair Credit Reporting Act (FCRA).

🔎 Monitoring: They offer fraud alerts and identity protection features (some free, some paid).

Is it 100% risk-free? No. No system is. But Experian is a legit financial institution that’s been around for decades. The real question is how you use it.

Is It Safe to Use Experian for a Credit Report?

If you’re just trying to see what’s on your credit file, you’re not exposing anything new—Experian already has that info. You’re just viewing it. Think of it like checking your attendance record in school—you’re not submitting anything, you’re just seeing what’s on file.

Just make sure you’re on the real Experian site or app (watch out for fake phishing links) and not sharing your login info.

Is It Safe to Use Experian Credit Score?

Yes—and checking it doesn’t lower your score. You’re performing what’s called a soft inquiry. This is completely safe and has no effect on your credit score. It’s different from a hard inquiry, which happens when you apply for a loan or credit card and a lender checks your credit report. Those can knock your score down a few points temporarily.

So if you’re just reviewing your score for your own awareness, it’s totally fine to check as often as you want.

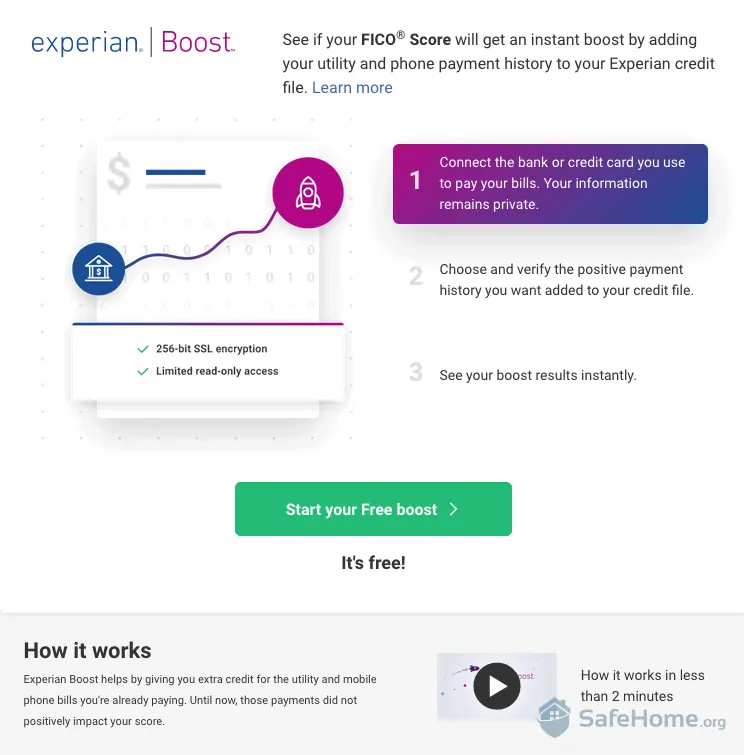

Is Experian Boost Safe to Use?

Experian Boost lets you link your bank account and earn credit for paying your bills—like your phone plan or Netflix—on time. It’s especially helpful if you’re just starting out and don’t have a traditional credit card or loan yet.

So, is it worth it?

They use encrypted, bank-level security.

It’s read-only access, meaning they can view your transactions but can’t move money.

You can disconnect your account anytime.

That said, if you’re super protective about who sees your bank info, you might not love the idea. But if you’re struggling to build credit, it’s a legit shortcut—and far safer than predatory lending or endless denials.

If Boost feels like too much, there’s another solid option: you could opt for a secured credit card to build credit, like Step. These work by using your own money as a deposit, so you’re not borrowing from a bank—you’re basically building credit by spending your own money, safely. And because secured cards report to the credit bureaus, they can help you grow your score over time, just like a regular credit card. It’s a low-risk way to get started without linking your bank or relying on someone else’s approval.

Is Experian Really Free? What You’re Signing Up For

Yes, but with limits.

You can:

Check your credit report and score for free

Get some basic credit alerts

Use Experian Boost at no cost

But there are premium features like identity theft protection, daily score updates, and advanced monitoring that cost extra. Just avoid accidentally enrolling in a free trial if you don’t want surprise charges.

How Your Experian Credit Report Helps You (or Not)

Your credit report isn’t just a number—it’s a detailed timeline of how you’ve handled money. Knowing what’s in it can help you:

Catch fraud

Fix errors that are hurting your score

Understand what lenders see before you apply

What’s Actually on an Experian Credit Report?

Your name, address, and employer history

Credit cards and loans (open and closed)

Missed or late payments

Public records like bankruptcies

Credit inquiries from lenders

It’s smart to review this regularly—especially before applying for something like an apartment or car loan.

FAQs About Experian

Does checking your score with Experian lower it?

Nope. That’s a soft inquiry—it doesn’t affect your score.

What is Experian’s credit score range?

Typically 300–850. A good score starts around 670.

Does your income affect your credit score?

No. Lenders care about income, but credit bureaus don’t track it.

Alternatives to Experian for First-Time Credit Builders

If Experian feels a little too complex, there are beginner-friendly options like Step.

Step is a credit building app designed for people 13+. There’s no credit check to sign up, and it helps you build credit with everyday purchases—like food, rides, or bills—through a secured card that reports to major credit bureaus.

It’s simple, transparent, and designed specifically for people figuring credit out for the first time.

Let’s be honest navigating the world of health insurance can feel like trying to solve a complex puzzle with a few missing pieces. With premiums, deductibles, and co-pays to consider, the sticker shock is real. The fear of rising healthcare costs often leaves people wondering if quality coverage is even within reach. The good news? It absolutely is.

Finding affordable healthcare isn’t about luck; it’s about knowing where to look and what to look for. Whether you’re self-employed, between jobs, or simply looking for a more budget-friendly option, you have more power than you think.

In this comprehensive 2025 guide, we will demystify the process and provide you with a step-by-step roadmap. We’ll break down everything you need to know to find the cheapest health insurance plans that don’t sacrifice essential coverage, giving you peace of mind for your health and your wallet.

Understanding What “Cheap” Really Means in Health Insurance

Before we dive in, it’s crucial to understand a key concept: the “cheapest” plan isn’t always the one with the lowest monthly premium. Your total healthcare cost is a balance between your monthly payment and how much you pay when you actually need care. It’s a trade-off you need to weigh carefully.

Here are the core terms you must know:

Premium: The fixed amount you pay every month to keep your insurance active. This is the most visible cost.

Deductible: The amount you must pay out-of-pocket for covered services before your insurance starts to pay. A lower premium often means a higher deductible.

Copayment (Copay): A fixed fee you pay for a specific service, like a doctor’s visit or a prescription, after your deductible is met.

Coinsurance: The percentage of costs you share with your insurance company for a covered service after you’ve paid your deductible.

The goal is to find a plan where this combination of costs is the lowest for your specific health needs. A young, healthy individual might save money with a high-deductible plan, while someone with a chronic condition might find a plan with a higher premium but lower out-of-pocket costs to be the most affordable option overall.

Your Step-by-Step Guide to Finding the Cheapest Health Insurance Plans

Ready to start the hunt for affordable coverage? Follow these actionable steps to uncover the best options available to you in 2025.

Step 1: Check Your Eligibility for Government Programs

Your first stop should always be to see if you qualify for free or low-cost coverage through government-sponsored programs. You might be surprised at what you’re eligible for.

Medicaid & CHIP: Medicaid provides comprehensive coverage to millions of low-income adults, pregnant women, and children. The Children’s Health Insurance Program (CHIP) offers low-cost coverage for children in families who earn too much to qualify for Medicaid but cannot afford private insurance. Eligibility is based on your household income and varies by state.

Marketplace Subsidies (Premium Tax Credits): This is the single biggest money-saver for most people. If you purchase a plan through the Health Insurance Marketplace, you may qualify for a premium tax credit based on your estimated income for the year. According to the Kaiser Family Foundation (KFF), these subsidies have made coverage significantly more affordable for millions of Americans. These credits directly lower your monthly premium, sometimes dramatically.

Step 2: Explore the Health Insurance Marketplace

The official Health Insurance Marketplace at HealthCare.gov is the central hub for comparing and purchasing plans. It’s designed to make finding affordable healthcare easier by standardizing plan information.

Plans on the Marketplace are categorized into four “metal” tiers:

Bronze: Lowest monthly premiums, but the highest deductibles and out-of-pocket costs. Best for healthy individuals who want protection from worst-case medical scenarios.

Silver: Moderate premiums and moderate deductibles. Crucially, if you qualify for cost-sharing reductions (CSRs), you can only get them with a Silver plan. CSRs lower your deductible, copays, and coinsurance.

Gold: High monthly premiums, but low deductibles and out-of-pocket costs. A good choice if you expect to need regular medical care.

Platinum: The highest premiums and the lowest out-of-pocket costs.

For those seeking the cheapest health insurance plans from a monthly premium perspective, Bronze plans are the obvious starting point. However, if you qualify for subsidies, a Silver plan could offer far greater value.

Step 3: Consider High-Deductible Health Plans (HDHPs) with an HSA

A High-Deductible Health Plan (HDHP) is exactly what it sounds like: a plan with a higher deductible than traditional plans. In exchange, you get a much lower monthly premium. This can be one of the most effective ways to secure a low-cost medical coverage option.

The secret weapon of an HDHP is its eligibility for a Health Savings Account (HSA). An HSA is a tax-advantaged savings account you can use for medical expenses. Here’s why it’s a powerful tool:

Triple Tax Advantage: Contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses are also tax-free.

It’s Your Money: Unlike an FSA, the money in your HSA rolls over year after year and is yours to keep, even if you change jobs or insurance plans.

Builds a Health Nest Egg: It can serve as a long-term investment account for future healthcare needs.

If you are relatively healthy and want to take control of your healthcare spending, an HDHP paired with an HSA is a fantastic way to get one of the cheapest health insurance plans available.

Step 4: Look into Short-Term and Catastrophic Plans (With Caution)

In certain situations, other types of low-premium plans might seem appealing. However, it’s vital to understand their limitations.

Short-Term Health Insurance: These plans offer temporary coverage, typically from a few months to a year. They have very low premiums but do not have to comply with Affordable Care Act (ACA) rules. This means they often don’t cover pre-existing conditions, maternity care, or mental health services. They are best used as a temporary bridge between other coverage.

Catastrophic Plans: Available only to people under 30 or those with a hardship exemption, these plans have very low premiums and extremely high deductibles. They are designed to protect you from financial ruin in a major medical emergency but offer minimal coverage for routine care.

Step 5: Compare Plans and Read the Fine Print

Once you’ve narrowed down your options, it’s time to compare. Don’t just look at the premium. Dig into the details:

Network: Are your preferred doctors and hospitals in the plan’s network? Going out-of-network can be incredibly expensive.

Prescription Drug Coverage: Check the plan’s formulary (list of covered drugs) to ensure your medications are included and affordable.

Total Out-of-Pocket Maximum: This is the absolute most you would have to pay for covered services in a year. A lower maximum provides better financial protection.

Conclusion: Your Path to Affordable Coverage

Finding the cheapest health insurance plans in 2025 is entirely possible when you approach it with a clear strategy. It’s not about finding a magic-bullet plan but about understanding your own needs and systematically exploring your options.

To recap, your path to affordable coverage involves checking your eligibility for subsidies, carefully comparing Marketplace tiers, weighing the benefits of an HDHP with an HSA, and always reading the details of a plan before you enroll. By investing a little time in research, you can secure a plan that protects your health without breaking your budget.

What are your biggest challenges in finding affordable health insurance? Share your questions and experiences in the comments below let’s help each other navigate this process!

Frequently Asked Questions

Are the cheapest health insurance plans always the best choice?

Not necessarily. A plan with the lowest monthly premium often has a very high deductible, meaning you’ll pay more out-of-pocket for services. The “best” plan is one that balances affordability with your expected healthcare needs. If you rarely see a doctor, a high-deductible plan might be the cheapest overall. If you have ongoing medical needs, a plan with a higher premium but lower cost-sharing could save you money in the long run.

Can I get affordable health insurance if I’m self-employed?

Absolutely. The Health Insurance Marketplace is a primary resource for self-employed individuals. You can apply for the same premium tax credits and cost-sharing reductions as anyone else based on your household income. Additionally, you can typically deduct your health insurance premiums as a business expense, further lowering your overall cost.

What’s the difference between an HMO and a PPO plan?

An HMO (Health Maintenance Organization) typically requires you to use doctors, hospitals, and specialists within its network and requires a referral from your primary care physician (PCP) to see a specialist. A PPO (Preferred Provider Organization) offers more flexibility, allowing you to see both in-network and out-of-network providers without a referral, though your costs will be lower if you stay in-network. HMOs often have lower premiums, while PPOs offer greater choice.

When is the open enrollment period for 2025?

The standard Open Enrollment Period for Marketplace health insurance typically runs from November 1st to January 15th in most states. However, you may be eligible for a Special Enrollment Period (SEP) outside of this window if you experience a qualifying life event, such as losing other health coverage, getting married, having a baby, or moving.

Life insurance is one of the smartest ways to protect your family’s financial future.

It guarantees financial support if something unexpected happens and gives peace of mind knowing loved ones will be cared for. With so many providers competing for your attention, finding the right policy can be overwhelming.

That’s why we’ve reviewed the Best 5 Life Insurance Companies in 2025. These insurers stand out for affordability, reliable coverage, and customer satisfaction. Whether you’re looking for term life, whole life, or flexible policies, these companies can meet your needs.

Why Choosing the Right Life Insurance Company Matters

The cost of life insurance can vary widely depending on age, health, and provider.

But choosing a trusted company isn’t just about premiums. It’s about financial stability, claims approval, customer service, and flexible options.

By sticking with the Best 5 Life Insurance Companies in 2025, you’ll save money and get dependable coverage when it matters most.

1. Northwestern Mutual

Northwestern Mutual has been around for more than 160 years and consistently earns the highest financial strength ratings (A++ from AM Best). This means customers can count on the company to pay claims reliably, even during economic downturns.

Features & Solutions:

Offers both term and permanent policies (whole life and universal life).

Dividends on whole life policies provide extra value.

Pros: Affordable term life, trusted reputation, wide coverage choices. Cons: Limited online quotes, requires working with an agent.

2. Prudential

Prudential is known for offering one of the largest selections of life insurance products in the U.S. This flexibility makes it easier to match coverage to your personal situation, whether you’re young and healthy or have complex health needs.

Features & Solutions:

Term life, whole life, indexed universal, and variable universal options.

Strong acceptance rates for applicants with medical conditions.

Customizable riders, like living benefits and accidental death coverage.

Pros: Wide range of policies, competitive for high-risk applicants, strong brand. Cons: Some policies can be more expensive, not always the cheapest for younger buyers.

3. State Farm

State Farm combines insurance coverage with a massive agent network across the U.S., which means customers get personal, one-on-one help. Its customer service ratings are consistently among the highest in the industry.

Features & Solutions:

Affordable term life policies that can be converted to permanent coverage.

Easy claims process with strong customer support.

Access to local agents for guidance on selecting and managing policies.

Pros: Excellent customer satisfaction, flexible options, great for families. Cons: Coverage amounts may be lower than some national providers.

4. MassMutual

MassMutual is one of the top Best Life Insurance Companies in 2025 for those who want affordable but reliable coverage. It combines strong financial ratings with budget-friendly policies that still provide excellent protection.

Features & Solutions:

Term life coverage starting as low as $100,000.

Online quoting system for quick comparisons.

Whole life policies with potential dividends for long-term value.

Pros: Affordable term life, financially stable, simple online process. Cons: Whole life policies are pricier, fewer digital tools than competitors.

5. Haven Life

Haven Life is a modern, digital-first insurer backed by MassMutual. It simplifies the process with a fast, online application that delivers instant decisions for many applicants. This makes it one of the most convenient options in 2025.

Features & Solutions:

Fully online application with instant coverage decisions.

Affordable premiums, especially for healthy and younger applicants.

Policies underwritten by MassMutual, giving extra financial security.

Pros: Quick and easy sign-up, transparent pricing, backed by a major insurer. Cons: Limited policy types, coverage may be restricted for older buyers.

Tips for Choosing the Right Life Insurance Company

Compare Quotes: Prices vary greatly, so shop around before you decide.

Check Financial Ratings: Always choose a company with a strong financial record.

Consider Your Goals: Term life works for affordability; whole life works for lifelong protection.

Look for Riders: Extra features like living benefits or critical illness riders can add valuable protection.

Think Long-Term: The Best Life Insurance Companies in 2025 are those that balance price, coverage, and dependability.

Conclusion

Life insurance is not just about numbers—it’s about peace of mind. By choosing from the Best 5 Life Insurance Companies in 2025, such as Northwestern Mutual, Prudential, State Farm, MassMutual, and Haven Life, you’re ensuring both affordability and reliability.

MassMutual delivers affordable term life coverage.

Haven Life offers a fast, online experience backed by a trusted brand.

The right choice depends on your needs, but all of these providers give you reliable coverage for the people who matter most. Investing in life insurance today means giving your family security and peace of mind for tomorrow.

Investing your money wisely is one of the best ways to build wealth and secure your financial future.

But with hundreds of firms competing for your attention, it can feel overwhelming to figure out where to start.

The good news? In 2025, investors have more choices than ever ranging from trusted global brands to new digital-first firms that make investing simple and affordable.

In this guide, we’ll review the best 5 investment companies in 2025 for safe, low-fee & high-return options.

Whether you’re a beginner looking for stability, or an experienced investor searching for higher growth opportunities, these companies are leading the way with smart solutions.

Why Choosing the Right Investment Company Matters

Not all investment companies are created equal Fees, investment choices, customer support, and technology can vary widely. so our article[ best 5 investment companies in 2025] will guide you step by step so continue reading peacefully

Even a small difference in annual fees can add up to thousands of dollars over time.

Likewise, the right company can give you tools, education, and portfolio options that align with your goals.

By focusing on the best 5 investment companies in 2025 for safe, low-fee & high-return options, you’ll reduce risk, keep more of your profits, and maximize long-term growth.

1. Vanguard

Vanguard remains a household name in 2025. Famous for introducing index funds, Vanguard continues to dominate because of its ultra-low expense ratios and investor-first philosophy.

Why it’s great:

Trusted brand, broad range of funds, excellent for retirement planning.

Best for: Long-term investors seeking stability and low fees.

Standout feature: Expense ratios often under 0.10%, making it one of the cheapest ways to invest.

if Best 5 investment companies in 2025 is discussed Vanguard should be the first to be mentioned

2. Fidelity

Fidelity is another top choice in 2025, offering everything from retirement accounts to trading platforms and even banking services. It balances low costs with strong customer service and advanced tools.

Why it’s great: Commission-free stock trading, zero-fee index funds.

Best for: Beginners and intermediate investors who want everything in one place.

Standout feature: Top-rated research tools and mobile app for easy investing.

3. Charles Schwab

Schwab is consistently ranked among the best investment companies in 2025 for safe, low-fee & high-return options.

It’s known for transparent pricing, great ETFs, and excellent customer support.

Why it’s great: Commission-free trading and low-cost ETFs.

Best for: Beginners who want an easy entry into investing.

Standout feature: Schwab Intelligent Portfolios, a robo-advisor service with no advisory fees.

4. BlackRock

BlackRock, the world’s largest asset manager, is another solid choice.

While it primarily serves large institutions, its iShares ETFs make professional-grade investing accessible to everyday investors.

Why it’s great: Wide variety of ETFs across industries and regions.

Best for: Investors looking to diversify into global markets.

Standout feature: iShares ETFs are among the most popular worldwide.

5. Betterment

For those who prefer hands-off investing, Betterment shines in 2025. It uses advanced algorithms to build and manage a diversified portfolio tailored to your goals.

Best for: Beginners or busy investors who don’t want to pick individual investments.

Standout feature: Low advisory fee (0.25%) and a focus on user-friendly design.

Tips for Choosing the Right Investment Company

Know Your Goals: Are you investing for retirement, buying a home, or short-term growth?

Compare Fees: Lower fees mean higher long-term returns.

Check Support & Tools: Look for research, education, and mobile access.

Diversify: Choose a company that offers a wide range of funds and assets.

Think Long-Term: The safest path is consistent investing with trusted firms.

Conclusion

The financial world is evolving quickly, but some names remain consistent leaders. Vanguard, Fidelity, Charles Schwab, BlackRock, and Betterment stand out as the best investment companies in 2025 for safe, low-fee & high-return options.

Each offers unique benefits, whether you want rock-bottom fees, powerful tools, or a completely automated experience.

At the end of the day, the “best” choice depends on your goals. If you want stability and low costs, Vanguard or Fidelity may be ideal. If you prefer automation, Betterment could be the smarter path. By partnering with one of these trusted companies, you’ll be taking a safe, smart step toward financial growth in 2025 and beyond.

{kind=link}